USDT cards are built for people who get paid, save, or move money in Tether and want a card-linked way to spend that value. You fund the account with USDT, the balance becomes available inside the card program, and the card converts value to the merchant's currency when the transaction is approved, that is different from paying merchants directly in raw on-chain USDT.

A good USDT card keeps three steps clear: how Tether gets in, how the card spends it, and how unused value can come back out. Supporting USDT is not enough on its own. A card can still be a poor choice if the cheapest deposit network is unclear, FX costs stack at checkout, refunds return to an unexpected destination, or withdrawals are harder than deposits.

Top Crypto Cards For USDT

- Fast virtual card access

- Broad stablecoin and crypto funding support

- Strong travel and cross-border utility

- Up to 4% back in XRP (U.S.).

- Spend 200+ assets with instant virtual card.

- No foreign transaction fees on Elite tier.

- Dual-mode spending — Switch between Debit Mode (spend balances) and Credit Mode (borrow against assets).

- No annual card fees — No monthly, annual, or inactivity fees on the card itself.

- Flexible crypto rewards — Earn cashback in NEXO tokens or BTC, depending on your preference and loyalty tier.

- Up to 10% Tiered Cashback – Competitive top-end rewards for high spenders and VIP users.

- Fiat-First Spend Logic – Uses fiat balance first, auto-converts selected crypto only if needed.

- Transparent Fee Structure (EEA program) – FX (0.5%) and crypto conversion (0.9%) fees are clearly disclosed rather than hidden in spreads.

- Stablecoin-led global spending

- Virtual and physical card access

- Card, wallet, transfers, swaps and credit in one app

KAST ranks first because it gives USDT users broad receive-network coverage, a simple card-spend path after top-up, and practical withdrawal options instead of trapping value only inside the card. RedotPay is the stronger alternative for users outside restricted regions who want app-based stablecoin payments and local payout routes. Nexo, Uphold, and Bybit are better fits when your USDT already sits inside those platforms and you accept their regional limits, conversion rules, and cash-out paths.

Comparison Table

| Name | Network | Card Type | Digital Wallets | Availability | Rating |

|---|---|---|---|---|---|

| | Visa | Prepaid | Apple Pay, Google Pay | 170+ countries, varies by jurisdiction. | 7.5Very Good |

| | Visa | Debit | Apple Pay, Google Pay | United States and the United Kingdom. In the U.S., the card is not available in New York, Louisiana, or U.S. territories. In the U.K., Crown Dependencies and British Overseas Territories are excluded. | 7.5Very Good |

| | Mastercard | Dual-mode | Apple Pay, Google Pay | Citizens and residents of selected European countries, including the EEA and the United Kingdom. | 7.1Good |

| | Mastercard | Debit | Apple Pay, Google Pay | Bybit Card is only available in limited countries and runs as separate regional card programs, including EEA and Switzerland, Australia, Argentina, Brazil, AIFC, parts of Asia Pacific, and Mexico. EEA residents may be directed to apply via Bybit EU for an EUR card | 6.5Good |

| | Visa, Mastercard | Prepaid | Apple Pay, Google Pay | 100+ countries, varies by jurisdiction. | 6.5Good |

This comparison narrows the list faster than rewards tables or branding comparisons. The real question is whether a card supports your specific network, your preferred card format, and a verification level you can actually complete.

Best USDT Cards By User Type

Some cards look close in a broad comparison but suit very different users. This section makes that split easier to see before you read the full reviews.

| User Type | Best Pick |

|---|---|

| Freelancer Paid In USDT | KAST Card |

| Traveler | RedotPay |

| Low-Friction Spender | KAST Card |

| Exchange-Native User | Bybit Card |

| User Who Needs Stronger Bank Off-Ramp | Uphold Card |

KAST covers most general-use cases because the spend flow is straightforward. Uphold stands out when bank movement matters more. Bybit only becomes the better choice when your money already lives inside that exchange.

Crypto Cards For USDT Reviews

Kast Card

Pros

- Virtual card is ready within minutes of approval, with no shipping wait required

- Apple Pay and Google Pay are supported from the start, so you can spend before the physical card arrives

- Stablecoin deposits (USDT, USDC, USDe, PYUSD, RLUSD) convert to USD at 1:1 with no spread

- The Standard tier costs nothing to open, which keeps the entry bar low for first-time users

- Visa acceptance and physical card delivery cover 170+ countries, which is a wider reach than most crypto cards offer

Cons

- Deposited crypto is treated as sold to KAST on entry, with no self-custody option inside the card flow

- Full KYC and partner approval can block or delay access, even for users in supported countries

- Non-USD spend adds a 0.5% to 1.75% FX fee on top of every transaction

- ATM withdrawals require the physical card, cost $3 plus 2% per transaction, and are capped at $750 per day

- Premium tiers start at $1,000 per year, which is hard to justify unless you spend a very high volume and want KAST Points and token rewards rather than cash

Uphold Card

Pros

- Up to 4% XRP rewards on Elite, with a promotional window for new U.S. applicants

- Spend from 200+ assets including fiat, stablecoins, and crypto from one wallet

- Instant virtual card with Apple Pay and Google Pay on both U.S. and U.K. accounts

- No annual fee on Essential

Cons

- Crypto-funded purchases carry a variable conversion spread that reduces net value

- U.S. rewards are XRP-only with no option to switch reward asset

- Essential tier has a $2,500 daily spend cap and $500 ATM limit

- Available only in the U.S. and U.K., with additional state and territory exclusions

Nexo Card

Pros

- Switchable Debit and Credit modes in one Mastercard.

- No monthly or annual card fees.

- Up to 2% cashback, paid in NEXO or BTC, depending on your tier.

- In-app spending controls and standard security features.

Cons

- Only available in selected European markets; not supported in the U.S.

- Cashback requires Credit Mode, a portfolio above $5,000, and a qualifying loyalty tier.

- FX fees apply even within EEA and UK, and the rate increases on weekends.

- Physical card ordering is temporarily paused, so the virtual card is the only option right now.

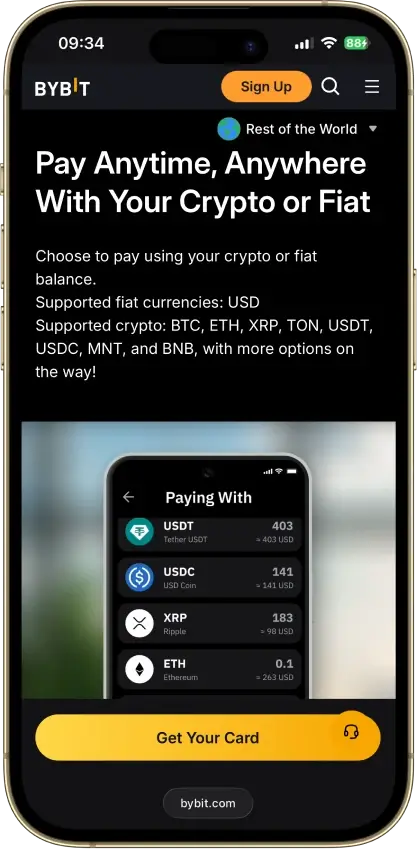

Bybit Card

Pros

- Up to 10% tiered cashback in Rewards Points.

- No annual, inactivity, or card cancellation fee

- Fiat-first spending can avoid crypto conversion fees.

- Strong card controls (freeze, limits, toggles).

Cons

- Limited country availability (no U.S.).

- 0.9% crypto conversion fee (EEA program).

- 0.5% FX on cross-currency spend (EEA program).

- Rewards are tier-based and capped monthly.

RedotPay

Pros

- Virtual card activates fast after KYC and funding, so online spend starts within minutes of approval.

- Physical card unlocks ATM access and in-store use, not just checkout payments.

- Apple Pay support means you can tap to pay in supported regions without carrying the physical card.

- No monthly or annual fee keeps the holding cost flat once you've paid the issuance fee.

- One app covers cards, wallet balances, transfers, swaps, P2P, and crypto-backed credit.

Cons

- Full KYC including ID upload and face scan is required before any core feature is accessible.

- Physical card issuance costs $100 and that fee is non-refundable.

- A 1.2% FX fee applies on every cross-currency transaction, including ATM withdrawals in a foreign currency.

- Custody sits with RedotPay and its partners, so balances can be frozen if compliance checks flag the account.

- The $50 chargeback fee and 3-to-6-month resolution timeline make disputes expensive and slow.

Our Ranking Methodology

These rankings score cards for USDT use, not generic crypto-card appeal. The highest-scoring card should make it easy to receive Tether, avoid wrong-network deposits, understand when conversion happens, spend reliably, and move unused value back out without disproportionate cost.

Rewards were not scored as a standalone category on this page. They only affected the ranking when they reduced real cost after caps, exclusions, plan fees, payout currency, and volatility. This page ranks usable USDT card flows first.

| Criterion | Weight | What We Measured |

|---|---|---|

| Availability And Setup Friction | 1.00 | Eligible countries, KYC level, approval friction, virtual-card access, physical-card access, and whether a new user can still apply |

| USDT Funding Rails And Network Risk | 1.50 | Supported USDT networks, cheapest practical deposit route, minimum deposits, wrong-network risk, and whether the app makes the route clear before sending |

| Spend Model And Checkout Conversion Clarity | 1.25 | Whether USDT stays as the funding asset, converts into an internal card balance, or converts at checkout; whether merchants receive fiat rather than raw USDT |

| Real-World Spend Reliability | 1.25 | Online spend, in-store spend, mobile-wallet use, merchant acceptance, subscriptions, pre-authorizations, travel use, and prepaid-card quirks |

| Fees And Hidden Stablecoin Cost Drag | 1.25 | Top-up costs, spread, crypto conversion, FX, ATM, issuance, replacement, withdrawal, inactivity, and partner fees |

| Cash-Out And Refund Practicality | 0.75 | Whether unused value can return to a wallet, bank account, or payout route; refund destination; refund timing; and whether withdrawals use the same network as deposits |

| App, Controls, And Card Tooling | 0.75 | Virtual card speed, physical card option, Apple Pay, Google Pay, freeze/unfreeze, spend controls, alerts, transaction history, and statement access |

| Security, Custody, And Freeze Risk | 1.25 | Custody model, issuer or partner clarity, sanctions and KYT checks, account-freeze risk, stablecoin handling, and whether funds sit with the card program or a partner |

| Support, Disputes, And Chargebacks | 0.50 | Human support routes, fraud reporting, dispute deadlines, chargeback fees, refund tracing, and review timelines |

| Tax And Reporting Readiness | 0.50 | Statements, CSV exports, transaction history, tax forms, cost-basis clarity, and whether crypto spending is explained as a possible taxable disposal |

The scoring favors cards that make the full USDT path clear: USDT in, spend model, fee drag, refund behavior, and money back out. A card can rank lower even with better brand recognition if its USDT network support, conversion path, or cash-out flow is harder to verify.

What Is A USDT Card and How Does It Work?

A USDT card lets you spend against a Tether balance instead of keeping only bank fiat on the card. In most setups, the merchant still gets paid in local currency, and the card program handles the conversion in the background when the transaction goes through.

How that conversion happens depends on the issuer. Some cards act like debit cards tied to a crypto balance. Some convert USDT at checkout. Others sit inside a larger account that supports both crypto and fiat. A few offer a credit mode where you borrow against crypto instead of spending it directly. The four most common setups break down like this:

- Direct spending uses USDT as the balance behind the card

- Auto-conversion turns USDT into local currency when you pay

- Debit-style cards pull value from your crypto balance, not a credit line

- Credit-style models use pledged crypto as collateral and settle later

That setup affects day-to-day use, fees, tax records, and how refunds come back to your account.

USDT Cards Fee

USDT cards are usually cheapest when you avoid unnecessary conversions and use the lowest-cost supported deposit route. The fees below focus on the costs that most often change the real spending value of a Tether balance.

KAST Card

- USDT top-up fee: 0% on stablecoin top-ups; 0% spread on stablecoin-to-USD balance conversion

- FX fee: 0.5% to 1.75% on non-USD transactions

- ATM fee: $3 plus 2%; non-USD ATM use can also add FX and operator fees on top

- Annual fee: $0 on Standard tier; paid tiers start at $1,000/year

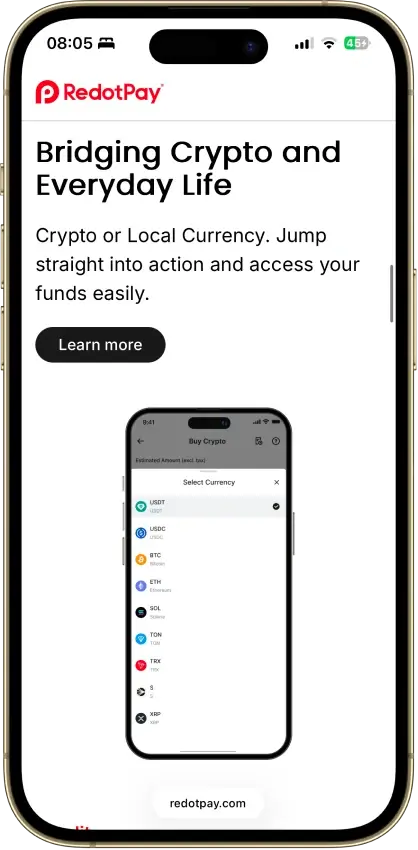

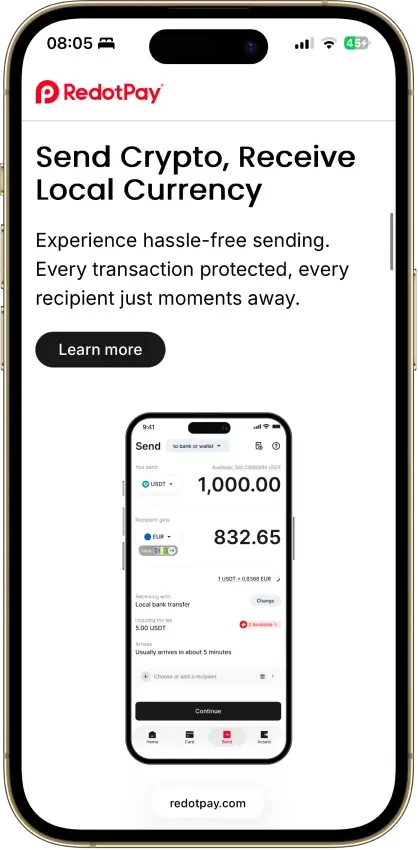

RedotPay

- USDT top-up fee: Listed as free on deposit; crypto handling or network costs may apply before crediting

- FX fee: 1.2% for non-default currency transactions; 1% crypto conversion fee

- ATM fee: 2%; USD card rises to 3% after $10,000 in monthly ATM withdrawals

- Annual fee: $0 for account maintenance; card application fees still apply

Nexo Card

- USDT top-up fee: No separate card top-up fee; USDT must be added to the Nexo account through supported asset-network routes

- FX fee: FX and asset-conversion costs can apply by region, mode, and timing

- ATM fee: Free monthly allowance applies; fees apply after limits

- Annual fee: $0 monthly, annual, or inactivity card fee

Uphold Card

- USDT top-up fee: No separate card top-up; fund the Uphold wallet by crypto network, bank, or card route

- FX fee: U.S. Essential: 1.50% foreign transaction fee; Elite: 0%; trading and spread costs can still apply

- ATM fee: U.S. Essential: $2.95; Elite: $0

- Annual fee: U.S. Essential: $0; Elite: $99.99/year

Bybit Card

- USDT top-up fee: Bybit does not charge on-chain crypto deposit fees; network fees still apply from the sender

- FX fee: EEA/CH program: 0.5%; regional programs differ

- ATM fee: EEA/CH program: 2% after the first 100 EUR/month; operator fees may apply

- Annual fee: None in the EEA/CH program

Use this section to screen for fee drag before checking rewards. A higher cashback rate can still lose value if USDT conversion, FX, ATM, or withdrawal costs are triggered often.

Worked Examples

These examples use realistic transaction amounts to show how fees actually stack. They are not projections.

Example 1 – Freelancer receiving 500 USDT and spending it in Europe (non-USD)

You receive 500 USDT via TRC20 and want to spend it in euros using a card.

- KAST: 0% top-up, 1.75% FX on a 200 EUR purchase = roughly 3.50 EUR in FX cost. Annual fee $0 on Standard.

- RedotPay: 0% top-up listed, 1.2% FX on the same 200 EUR = roughly 2.40 EUR. Card application fee applies once at setup.

- Bybit: 0% deposit fee from Bybit's side, 0.5% FX on 200 EUR = roughly 1.00 EUR. Only practical if your USDT already sits in Bybit.

- Nexo: No top-up fee, but FX and conversion costs depend on region and mode – exact amount requires checking in-app before spending.

- Uphold Essential: 1.50% foreign transaction on 200 EUR = roughly 3.00 EUR, plus any spread from the USDT-to-USD conversion step.

For a straightforward non-USD spend, Bybit has the lowest stated FX cost, but only if you are already inside the Bybit ecosystem. For someone depositing fresh USDT, KAST and RedotPay are the more accessible options, with RedotPay slightly cheaper on FX at standard rates.

Example 2 – Occasional ATM withdrawal of 200 USD equivalent

You want to withdraw 200 USD equivalent from an ATM once per month.

- KAST: $3 flat fee plus 2% = $7.00 per withdrawal, before operator fees.

- RedotPay: 2% = $4.00, rising to 3% after $10,000 monthly ATM volume (unlikely for casual use).

- Bybit (EEA/CH): 2% after the first 100 EUR free monthly. On a 200 EUR equivalent withdrawal, the first 100 is free and the remaining 100 is charged at 2% = roughly 2.00 EUR.

- Nexo: Free ATM allowance applies monthly; fees kick in above the threshold, which must be confirmed in-app.

- Uphold Essential: $2.95 flat per withdrawal. Elite tier: $0.

For occasional ATM use, Bybit's free first-100-EUR monthly allowance and Nexo's free allowance are the lowest-friction options – provided you are in an eligible region.

USDT Deposit Networks and Cheapest Routes

The cheapest USDT route depends on the exact asset-network pair shown inside the app. Do not send Tether just because the chain name appears elsewhere on the platform; the card or account must support USDT on that specific network.

| Card | Supported USDT Deposit Networks | Cheapest Network To Check First |

|---|---|---|

| KAST Card | Ethereum, TRON, Solana, Polygon, Arbitrum, BNB Chain | Solana or TRC20, depending on sender support |

| RedotPay | Main app supports USDT network deposits such as TRC20, ERC20, and BEP20; Mini App supports TON separately | TRC20 in the main app; TON only if using the Mini App flow |

| Nexo Card | Nexo supports USDT on selected account networks; exact top-up routes are shown in-app | TRC20 or Polygon if available; avoid ERC20 for small transfers |

| Uphold Card | Multiple crypto-network routes are available through the Uphold deposit screen; exact USDT route must be confirmed in-app | Varies by region and asset screen |

| Bybit Card | Bybit exchange deposit routes shown on the USDT asset page; common USDT routes include TRC20, ERC20, BSC, and Polygon/MATIC where available | TRC20 when available |

For small USDT top-ups, TRC20 is usually the first route to check because it is widely supported and typically cheaper than ERC20. Solana, Polygon, BSC, or TON can be cheaper in some flows, but only use them when the exact USDT route is confirmed for that card or account.

Direct USDT Spending vs. Auto-Conversion

Two cards can both support USDT and still behave differently after you top up. The important question is whether USDT remains a selectable funding asset until payment or whether it is converted into an internal fiat or card balance before the spend happens.

Three models cover most of the cards on this page:

- USDT-funded spending: Tether is the asset or source balance behind the card flow

- Checkout conversion: the card program converts enough value into the merchant's currency when the purchase is approved

- Pre-converted balance: USDT is converted into an internal USD, EUR, GBP, or other card balance before you spend

For most users, the best model is the one that makes deposits, checkout costs, refunds, and withdrawals easiest to track.

What To Check Before Choosing A USDT Card

Before picking a USDT card, narrow the decision to the things that actually change day-to-day use. That removes cards that look fine in a feature list but become awkward once you start paying with them.

These are the questions that matter most before you apply:

- Do you want USDT kept as the funding asset until checkout, or converted into an internal card balance first?

- Which USDT network will you actually use?

- Do you need Apple Pay or Google Pay?

- Do you need a physical card or is a virtual card enough?

- Do you need ATM access?

- Are you okay with full KYC?

- Will you keep only a spend balance there, or more?

These checks narrow the list faster than cashback rates or feature badges. They tell you whether the card stays usable after signup, not just whether it looks good in a comparison row.

Availability, KYC and What Each Card Requires

USDT support says nothing about how much verification a card requires. The more useful question is what each card asks for, what verification unlocks, and how regional issuance changes what you can do with the account.

KAST Card

- KYC level: Level 1 at signup; Level 2 required for card use

- What you submit: personal details, government ID, live selfie; proof of address if asked

- What verification unlocks: Level 1 opens the app and basic receive functions; Level 2 unlocks sending, receiving, virtual card, and physical card

- Region notes: country and residency checks apply; card support varies by market

RedotPay

- KYC level: full individual KYC

- What you submit: personal details, original government ID, face scan; personal statement if requested

- What verification unlocks: full account use and card application

- Region notes: not available in the US; one verified account per person

Nexo Card

- KYC level: identity verification on the Nexo account

- What you submit: personal details, country and address, government ID, selfie, regulatory information

- What verification unlocks: access to Nexo products, crypto top-ups, and card use in supported countries

- Region notes: selected European countries only, including the EEA and UK; physical card orders are paused

Uphold Card

- KYC level: fully verified Uphold account required

- What you submit: personal details, phone, government ID, selfie; financial details or source-of-funds prompts may appear

- What verification unlocks: trading, funding, withdrawals, and debit card access in supported regions

- Region notes: card available in the US and UK; excludes New York, Louisiana, US territories, Crown Dependencies, and British Overseas Territories

Bybit Card

- KYC level: identity verification plus card-region checks

- What you submit: government ID; proof of address or valid residential address in many card programs

- What verification unlocks: card application, funding, and spending in eligible regions

- Region notes: issuance depends on the regional card program, so supported countries and document checks vary

KYC is not only a signup issue. It determines when the card becomes usable and when limits move. Unusual activity, larger transfers, or account reviews can still trigger additional checks after the initial verification is complete.

Virtual Card vs. Physical Card for USDT Spending

A virtual card is enough for many people if the main goal is online spending or phone-wallet payments. When Apple Pay or Google Pay works in your region, a virtual card covers most day-to-day use without waiting for plastic delivery.

A physical card adds value when you need ATM access, an international travel backup, or a second payment option if phone-wallet acceptance fails. It also matters more in places where tap-to-pay coverage is weaker or merchants still require a card insert. Here is how to think through the choice:

- Online purchases: a virtual card is usually enough

- Apple Pay / Google Pay: virtual cards work well if wallet support is live in your region

- In-store tap-to-pay: a phone wallet can cover this, but acceptance is not consistent across every merchant setup

- Travel backup value: a physical card is more reliable if your phone dies or wallet acceptance fails

- Whether a physical card is worth getting if the virtual card already works: yes, if you want ATM access, a travel backup, or a second payment path

Where USDT Cards Usually Fail

USDT cards usually fail at the points where the crypto rail, card rail, and compliance rail do not line up. The card may work for a normal purchase and still become awkward when a deposit uses the wrong network, a merchant places a hold, or a refund returns differently than the original payment.

The most common failure points are worth knowing before you load funds:

- Deposit network mismatch: USDT exists on multiple chains. Sending TRC20, ERC20, BEP20, Solana, TON, or another version to the wrong route can delay or permanently lose funds.

- Hidden FX drag: a card can advertise free card spending while still charging crypto conversion, FX, weekend, ATM, or network withdrawal costs.

- KYC friction: card access can require higher verification than simple account signup, and larger transfers or unusual activity can trigger another review.

- Refund destination uncertainty: refunds may return as fiat balance, card balance, or the original asset depending on the program and settlement route.

- Cash-out friction: some products are easy to spend from but slower or more expensive when you try to move unused value back to a wallet or bank.

- Expensive ATM use: ATM withdrawals often add card fees, operator fees, FX fees, and low daily caps.

Treat a USDT card as a spend tool, not a long-term storage wallet. Test the deposit route, make one small purchase, confirm withdrawal options, and keep a bank card available for hotels, fuel holds, subscriptions, and disputes.

Common USDT Crypto Card Problems and Fixes

Most USDT card problems do not come from the coin itself. They come from the payment layer, the card program, or how the balance was funded before the transaction started. Each of these has a practical fix:

- Wrong-network deposit: check the supported network before sending and use a test transfer for any new route.

- Merchant decline: some merchant types, pre-authorizations, or risk filters can fail even with a sufficient balance.

- Refund delay: card refunds often take longer to settle than wallet transfers, so allow extra time before raising a dispute.

- Cash-out friction: a card that works well for spending can still add steps when you try to move unused funds back out.

- Extra KYC review: spending limits or withdrawal blocks often appear when users try to unlock higher tiers or additional card features.

- Travel checkout issues: FX fees, merchant category blocks, and offline terminals can all create friction on the road.

The safer approach is to treat a USDT card as a spending tool rather than a place to hold significant funds. Start with small amounts, keep a backup payment method, and check how the card handles refunds and withdrawals before loading more.

Tether Price and News

USDTTether News

Tether freezes 134 wallets as stablecoins now sit inside the sanctions machine

The 134-address action exposes how public-chain intelligence and issuer controls are becoming real-time enforcement infrastructure.

Tether trades 8.5% above India’s dollar rate as policy pressure hits USDT access

USDT gets a Brazil payment route to 170 million people by making crypto disappear