IBIT ETF vs Bitcoin: Which is the Best Way to Invest?

Should you buy BlackRock’s IBIT ETF or just stick with Bitcoin itself? It’s a question more and more investors are asking as crypto becomes a mainstream asset class.

In 2025, IBIT has seen record-breaking inflows, making it one of the most popular Bitcoin ETFs on the market. For many, it offers easy access to BTC exposure through a brokerage account — no wallets, no seed phrases, no fuss. But with that convenience comes trade-offs.

Do you value direct ownership and the ability to self-custody your Bitcoin, or would you rather have simplicity? In this article, we’ll break down how IBIT stacks up against holding actual Bitcoin so you can decide which fits your strategy best.

Key Takeaways: Should You Invest in the IBIT ETF or Bitcoin?

In short, IBIT is ideal for investors who want easy, regulated exposure through traditional accounts, while Bitcoin appeals to those who value full ownership and crypto-native utility. Many long-term believers prefer holding BTC directly, whereas newcomers or those investing via retirement accounts likely favor the ETF.

For a quick overview, here’s how the IBIT ETF vs Bitcoin stack up. The table below highlights their key differences and who each option may suit.

| Feature | IBIT ETF (BlackRock’s iShares Bitcoin Trust) | Bitcoin (BTC) – Direct Ownership |

| Asset |

|

|

| Underlying Exposure |

|

|

| Expense Ratio / Carry Cost |

|

|

| Trading Venue & Hours |

|

|

| Minimum Trade Size |

|

|

| Custody Method |

|

|

| Dividend / Yield |

|

|

| Regulatory Status |

|

|

| Security Risks |

|

|

In summary, IBIT is best suited for investors who want Bitcoin exposure without the technical hassle. It fits nicely in traditional portfolios – you can buy it in a 401(k)/IRA, get SIPC protection up to $500k on your brokerage account, and even use it as collateral for loans in some cases (for example, JPMorgan accepts IBIT shares for loans).

On the other hand, buying Bitcoin directly is ideal for those who believe in “being your own bank”. Direct BTC holders can self-custody offline, avoid ongoing fees, and use Bitcoin in ways an ETF can’t – from making payments on the Lightning Network to participating in DeFi protocols and any new on-chain innovations.

Many long-term holders choose Bitcoin itself for the ultimate control and alignment with crypto’s decentralized ethos.

What Is IBIT?

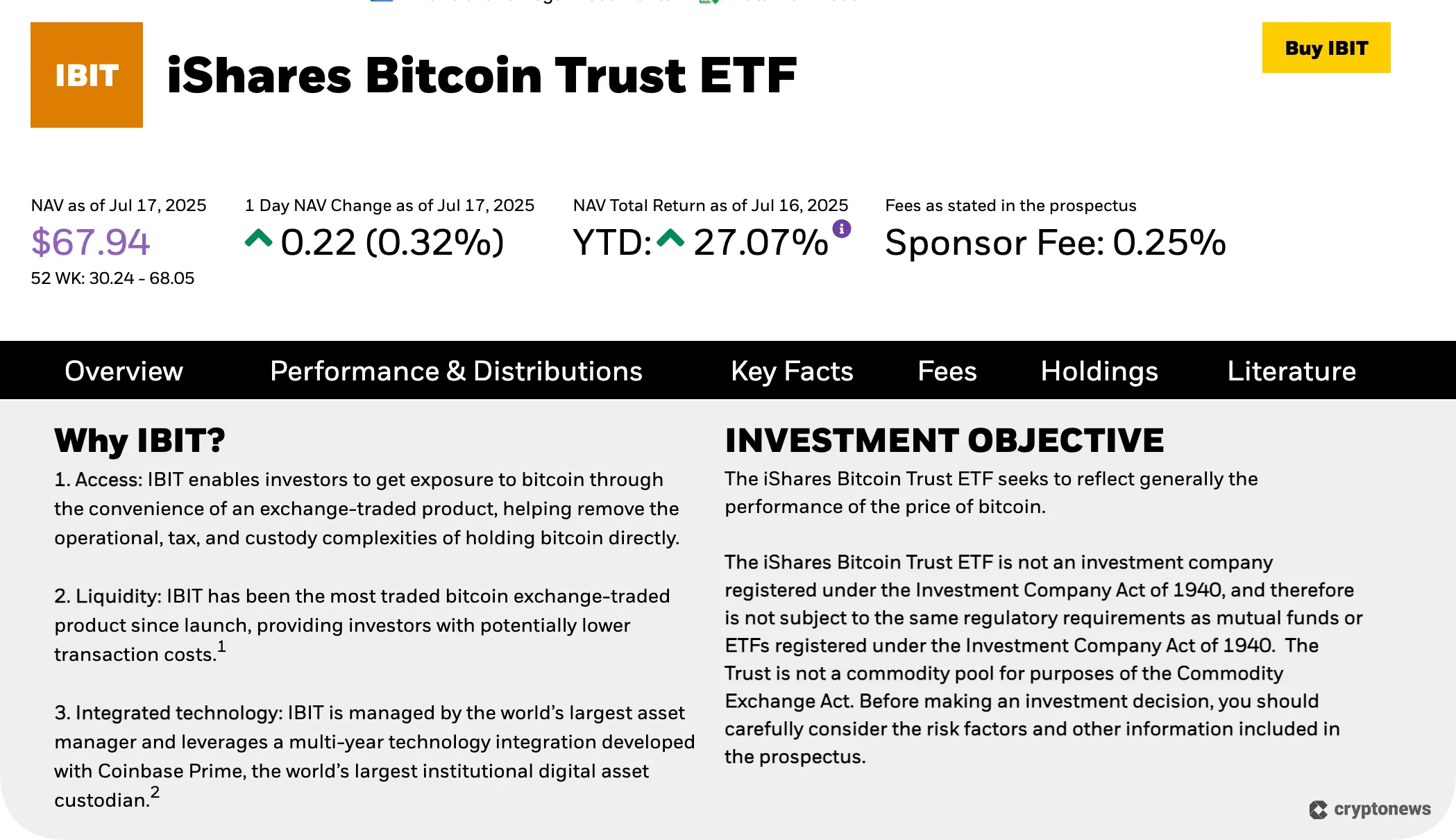

BlackRock’s spot Bitcoin ETF, IBIT, launched in January 2024. It holds actual Bitcoin in cold storage via Coinbase Custody. You buy shares representing fractional BTC ownership. This lets you access Bitcoin through your stock brokerage without directly managing wallets or private keys. It trades on the Nasdaq like any stock.

IBIT charges a 0.25% annual expense ratio. You pay no dividends since Bitcoin generates no income. You’ll receive a 1099-B form from your broker for tax reporting when you sell shares. This simplifies taxes versus holding Bitcoin yourself. The fee structure is clearer than older crypto trusts.

By mid-2025, IBIT held over 790,000 BTC. It operates under the Securities Act of 1933 as a trust. While not a traditional ’40 Act fund, regulators oversee its custody and transparency. Its growth proves strong institutional adoption. You gain exposure without direct asset management responsibilities.

Does IBIT Hold Actual Bitcoin?

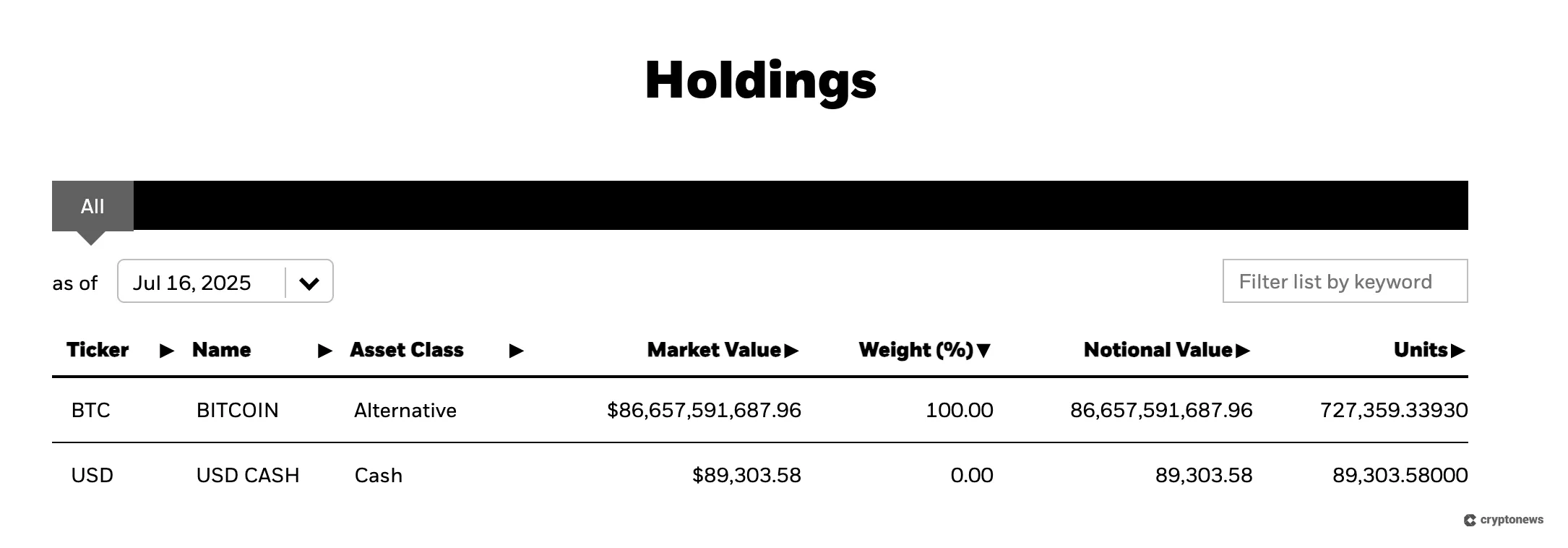

Yes, IBIT holds real, physical Bitcoin on-chain to back every share 1:1. You get daily proof of reserves: BlackRock and Coinbase publish the trust’s Bitcoin addresses and total holdings. This transparency lets you verify that actual BTC backs your investment. It operates like gold ETFs – Bitcoin is vaulted for you.

Authorized participants create or redeem shares for Bitcoin, keeping IBIT’s price aligned with Bitcoin’s market value. When you buy shares, new ones can be created; selling triggers redemptions. This daily process ensures minimal tracking error. The fund’s BTC holdings always match shares outstanding.

Unlike futures, ETFs (such as BITO), IBIT holds actual Bitcoin, not derivatives. Futures ETFs suffer roll costs and tracking gaps; spot ETFs like IBIT avoid these. Holding real coins also enables stronger security (insured cold storage) and purer Bitcoin exposure for you, without crypto wallets.

👉 Check here for the Best Cold Storage Crypto Wallets for 2026

What Does it Mean to Own Bitcoin Directly?

Direct Bitcoin ownership means you hold private keys, giving complete control over your coins. Use hardware wallets (like Ledger) or multi-signature setups for security. You manage everything – backups, transfers, and protection. Lose your keys? Recovery is impossible. This demands responsibility but ensures true sovereignty over your assets.

Self-custody puts you in charge. Store BTC in hardware wallets (offline devices), multi-sig vaults (shared key control), or trusted software. Unlike ETFs, you physically possess your Bitcoin. Trade-offs exist: convenience decreases as security increases. Always back up your 24-word recovery phrase offline.

Self-custodied BTC unlocks real utility beyond price speculation:

- Use Lightning Network for instant payments

- Earn yield via Bitcoin DeFi protocols

- Mint NFTs (Ordinals/Runes)

- Access cross-chain applications

- Claim forked coins (Bitcoin Cash)

- ETF shares can’t replicate these functions.

You avoid ongoing fees like IBIT’s 0.25% annual cost, saving around $250/year per $100k invested. Your BTC can’t be frozen; participate in governance or airdrops. The downsides are that you pay network fees ($0.50-$5/transaction) and cover security costs ($150 hardware wallet, for example). No institution mediates your transactions.

You become your bank, facing risks like phishing attacks targeting seed phrases or physical wallet theft. No fraud reversal exists (unlike credit cards). Mitigate threats with encrypted backups and multi-sig setups. New investors often find this overwhelming – ETFs simplify custody but sacrifice control and utility.

Choose direct ownership if you value censorship resistance: use Bitcoin actively, understand blockchain basics, and accept irreversible error risks. Prefer convenience? ETFs remove technical burdens but limit Bitcoin’s native functionality. Your goals – sovereignty versus simplicity – determine the optimal approach for holding Bitcoin.

IBIT Price vs Bitcoin: How They Track Each Other

IBIT maintains near-perfect Bitcoin tracking through its creation/redemption system. Authorized participants arbitrage price gaps:

- Create baskets (40,000 shares) by depositing BTC when IBIT trades at a premium

- Redeem baskets for BTC when IBIT trades at a discount

- This mechanism keeps IBIT’s price below a 0.1% tracking error versus actual Bitcoin.

Empirical data confirms exceptional alignment. From Q4 2024 to Q4 2025, IBIT rose nearly 54% versus Bitcoin’s 55% gains – a minor gap reflecting its 0.25% annual fee. Daily arbitrage eliminates deviations quickly. Bid-ask spreads average around 0.02%, ensuring you pay minimal trade costs.

IBIT and Bitcoin charts are virtually identical. Rallies, dips, and volatility match closely, unlike older products like GBTC that suffered large premiums and discounts. You avoid meaningful “fund price” risk. One limitation: IBIT trades only during market hours (9:30 AM-4 PM ET), while Bitcoin moves 24/7.

Overnight and weekend Bitcoin swings cause IBIT gaps at open, but arbitrage corrects prices rapidly. For example, a 5% weekend BTC surge would make IBIT jump 5% at Monday’s open. This timing difference doesn’t impact long-term holders.

Why tracking matters: You get Bitcoin’s core returns with minimal drag. High liquidity (over $10 million in daily volume) keeps spreads tight. Over 18 months, IBIT has delivered nearly identical exposure to holding BTC directly, minus the custody hassle.

For IBIT ETF price prediction, expect it to mirror Bitcoin’s trajectory minus fees. Its design ensures this. If Bitcoin hits $200,000, IBIT should follow closely, likely trading between $199,500-$200,500 per equivalent BTC share.

How Many IBIT Shares Equal 1 Bitcoin?

IBIT shares represent fractional Bitcoin ownership. As of mid-2025, each share equals roughly 0.00057 BTC, meaning approximately 1,754 shares equal 1 full Bitcoin. This ratio comes from BlackRock’s disclosures. For example, 40,000 shares correspond to about 22.72 BTC. Small daily fluctuations occur due to fees and share creation/redemption activity.

This structure lets you buy precise fractional exposure. One $36.23 IBIT share equals around 0.00057 BTC, so even a $50 purchase is fractional Bitcoin. Large authorized participants can swap share blocks for actual BTC, though retail investors cannot redeem directly. To convert your shares to BTC equivalent: multiply the share count by 0.00057.

Ultimately, IBIT shares economically mirror owning Bitcoin. The current ratio helps you align holdings (for example, 875 shares ≈ 0.5 BTC). Price shifts always reflect Bitcoin’s market moves minus minimal fees, making IBIT a precise proxy for spot BTC exposure without handling custody yourself.

IBIT vs Bitcoin: Key Differences Explained

Now let’s dive deeper into specific dimensions where holding IBIT or Bitcoin differs. Both choices give you Bitcoin price exposure but differ in how you realize that exposure and what additional benefits or drawbacks come along.

Below, we break down fees, custody, accessibility, liquidity, and taxes for IBIT vs. BTC.

Fees and Total Cost of Ownership

IBIT charges a 0.25% annual management fee, deducted daily from its value. You may also pay tiny bid/ask spreads (around 0.02%) when trading shares. Broker commissions are often $0.

This fee covers custody and administration, but slowly compounds over time, costing ~2.5% over a decade if Bitcoin doesn’t appreciate.

Direct Bitcoin ownership avoids recurring fees. You pay:

- Exchange trading fees (0.1%-0.5% per buy/sell)

- Network withdrawal fees ($0.50-$5)

- Optional hardware wallet ($50-$150 one-time)

- After purchase, holding BTC costs nothing unless you add services like custodial insurance.

For infrequent traders, direct Bitcoin saves long-term costs, which means no annual drag. Frequent traders might spend more than 0.25% on exchange fees. IBIT consolidates costs for regular investors but guarantees a fee regardless of performance. Choose Bitcoin for minimal fees if you self-custody; pick IBIT for simplicity despite its annual cost.

Custody and Security Risks

IBIT delegates custody to BlackRock and Coinbase – you never hold personal keys. Coinbase secures Bitcoin via cold storage and multi-signature protocols. Your brokerage account includes SIPC protection ($500k against broker failure), reducing personal risk. However, you trust these institutions entirely and accept potential regulatory or operational risks outside your control.

Direct Bitcoin ownership gives you complete control but demands rigorous security discipline. You must safeguard private keys using hardware wallets, offline backups, and phishing awareness. Mistakes like lost seed phrases are irreversible: no insurance exists. The upside? No third-party risks (exchange collapses, asset freezes) if you manage keys properly.

Choose IBIT for institutional-grade security without effort. Opt for Bitcoin if you prioritize sovereignty and accept personal responsibility. Neither eliminates risk: IBIT involves trusting institutions, while Bitcoin relies entirely on your security practices. The core trade-off remains convenience versus absolute control over your assets.

Accessibility and Use Cases

IBIT integrates seamlessly into traditional finance. You trade it like stocks through brokers (Fidelity, Schwab). It fits IRAs/401(k)s and supports margin trading and options strategies. This simplifies Bitcoin exposure for conventional investors but limits functionality – you can’t spend IBIT or interact with blockchain networks. It’s purely an investment vehicle.

Direct Bitcoin offers actual ownership and broader utility:

- Borderless transfers (send globally 24/7)

- Programmable money (DeFi, lending, Lightning Network)

- Sovereign asset control (no intermediaries)

- Unlike IBIT, BTC works as currency and integrates with crypto ecosystems.

Choose IBIT for easy, regulated exposure in brokerage accounts. Pick Bitcoin if you value self-custody, global payments, or participating in crypto innovations. IBIT suits passive investors; BTC empowers active users of decentralized technology.

Liquidity and Trading Hours

IBIT trades exclusively during Nasdaq market hours (9:30 AM–4 PM ET, weekdays). It offers excellent liquidity with tight spreads when markets are open. However, you face gap risk. Bitcoin’s off-hour price moves (such as weekend surges) won’t reflect in IBIT until trading resumes. After-hours access is limited and less liquid.

Bitcoin trades 24/7 globally on exchanges like Coinbase and Binance. With deep liquidity, you can buy/sell anytime and react instantly to news. This constant access means no forced waiting periods and no breaks from volatility – your portfolio moves even overnight or on holidays.

Choose IBIT for high liquidity within traditional market windows. Prefer Bitcoin for uninterrupted, global 24/7 trading access. IBIT suits scheduled traders; Bitcoin empowers those needing constant market access despite its non-stop price action. Both handle large orders efficiently during active hours.

Tax Implications

IBIT is taxed like securities. Your broker provides a 1099-B form for sales, simplifying reporting. Wash-sale rules apply – you can’t claim losses if repurchased within 30 days. It fits seamlessly in IRAs/401(k)s for tax deferral. No transaction tracking is needed, but you lose loss-harvesting flexibility.

Direct Bitcoin requires self-reporting. You file Form 8949 for every sale, trade, or purchase. No wash-sale rule exists (yet), letting you harvest losses and immediately rebuy. However, frequent use creates complex tracking. Gifting and donations offer tax benefits but add paperwork.

Choose IBIT for automated reporting and retirement accounts. Prefer Bitcoin only if you’ll leverage loss-harvesting or accept meticulous record-keeping. IBIT’s simplicity suits most, while Bitcoin’s flexibility demands discipline. Long-term gains rates apply to both after over 1 year of holding.

Why Some Investors Prefer IBIT

Given the above differences, why choose IBIT over Bitcoin? Here are the key reasons some investors opt for the ETF:

- Simplicity and familiarity: IBIT offers simplicity for traditional investors – buying it works like stocks in your brokerage. You skip learning about wallets or blockchain tech. Professionals handle Bitcoin custody and transactions behind the scenes. This convenience appeals to those wanting exposure without crypto complexity.

- Traditional investment integration: IBIT integrates seamlessly into existing portfolios. Hold it in SIPC-protected brokerage accounts (up to $500k coverage) or retirement funds like IRAs. It supports margin, lending, and risk tools (stop-loss/options). This “financializes” Bitcoin into a conventional asset, with protections unavailable on crypto exchanges. Brokerage infrastructure handles all settlements securely.

- No key management: No need to manage private keys –BlackRock’s experts handle security. You eliminate risks like forgotten passwords, sending to the wrong addresses, or exchange hacks. This outsourcing removes the technical burden and “human error” worries. Ideal for investors who prioritize ease: exposure without operational headaches.

- Regulated and trusted parties: Backed by BlackRock and SEC oversight, IBIT operates within clear regulatory frameworks. This reassures conservative investors wary of crypto’s legal uncertainty. By mid-2025, its volatility stabilized to match S&P 500 ETFs, signaling mainstream acceptance. Institutions trust their compliant, audited structure over direct crypto.

- No direct exposure to crypto platforms: IBIT avoids crypto exchanges entirely. You transact through familiar brokers via traditional settlement (DTC), bypassing risks like FTX-style collapses or unregulated platforms. Your assets never touch crypto ecosystems, which is ideal for those skeptical of the “wild west” of digital asset exchanges.

In summary, IBIT is preferred by those who want ease, security, and integration with traditional finance. It transforms Bitcoin into something that looks and feels like buying an ETF, which for many is the only way they are comfortable participating. It’s bringing Bitcoin to the masses who would never deal with a crypto wallet. As a result, IBIT has massively broadened Bitcoin’s investor base, drawing in pension funds, advisors, and everyday investors who trust the ETF format.

Why Some Investors Prefer Bitcoin

Conversely, many crypto veterans and believers will tell you: “If you want to invest in Bitcoin, just buy Bitcoin”. Here’s why some prefer holding BTC directly:

- Sovereignty and self-custody: Direct Bitcoin ownership ensures sovereignty and self-custody – you control your assets without intermediaries. No institution can freeze or seize your coins. This aligns with Bitcoin’s core purpose: genuine financial autonomy. IBIT relies on BlackRock, contradicting this principle. Your private keys mean ultimate authority, eliminating third-party dependency.

- No ongoing fees or middlemen: Zero ongoing management fees preserve wealth long-term. Avoiding IBIT’s 0.25% annual fee compounds savings during appreciation. Costs are limited to one-time expenses like hardware wallets. Unlike ETFs, Bitcoin carries no fund mismanagement risk – you own the asset directly. You keep 100% of the gains without intermediaries.

- Access to protocol-level innovation: Direct BTC grants access to Bitcoin’s protocol innovations, including Ordinals NFTs, Lightning Network payments, and staking via sidechains. You participate in ecosystem upgrades like smart contracts, which IBIT holders cannot engage in. Real Bitcoin enables full utility: payments, DeFi, and future developments are impossible through ETFs.

- Privacy potential: Self-custodied Bitcoin offers greater privacy than IBIT. Brokerages track all ETF trades via KYC; Bitcoin allows pseudonymous methods like coinjoin. IBIT subjects its holdings to regulatory scrutiny. Direct ownership lets you control financial visibility, critical for privacy-focused users avoiding surveillance.

- Avoiding counterparty and regulatory risk: Eliminate ETF-specific risks: no exposure to BlackRock’s operations, regulatory shifts, or redemption halts. Self-custody removes intermediaries – your BTC isn’t vulnerable to fund failures. Actual ownership means no third party stands between you and your asset’s security.

- Cultural/ideological preference: Direct ownership honors Bitcoin’s anti-establishment ethos. Many reject Wall Street products like IBIT on principle. Self-custody embodies empowerment and aligns with decentralized values. Holding physical BTC (not an IOU) is the authentic expression of “your keys, your coins.”

In summary, investors prefer Bitcoin when they value control, pure exposure, and the potential to do more with their asset than just holding it for price. They’re willing to take on the complexities of self-custody in exchange for not relying on any third party.

For those who genuinely believe in Bitcoin’s long-term significance, holding the real thing is often seen as the more authentic and potentially more rewarding way (both financially and philosophically) to invest.

Who Should Own IBIT, Bitcoin, or Both?

Choosing between IBIT and Bitcoin doesn’t have to be an all-or-nothing decision. Different investment goals may call for other formats – in fact, some investors hold both IBIT and BTC for complementary benefits. Here’s a quick guide:

- Traditional investors → IBIT. If you’re a conventional investor (individual or institution) who wants exposure to Bitcoin’s price with minimal disruption to your current processes, IBIT is ideal. It’s great for those using retirement accounts, those who need the blessing of compliance departments, or anyone uncomfortable with managing digital wallets. IBIT gives easy access to Bitcoin’s upside, in a familiar wrapper, and integrates with stocks/bonds in a portfolio.

- Long-term Bitcoin believers/HODLers → Bitcoin Direct. If you intend to accumulate Bitcoin as a long-term store of value or align with crypto’s ethos, holding BTC directly is the way to go. You can take self-custody, eliminating ongoing fees and third-party risks. This is suited for those who don’t mind (or even relish) taking responsibility for security and want the ability to use Bitcoin in the future. Long-term HODLers often prefer owning the underlying asset they can control 100%.

- Active Traders or Hedgers → Possibly Both. More advanced investors might use a combo approach. For example, you could hold Bitcoin in cold storage for the ultra-long term (your “never sell” stash), and use IBIT in a brokerage for short-term trading or in tax-advantaged accounts. Some might also arbitrage between the two if any price dislocations occur. Both give flexibility: IBIT for when you need liquidity or to raise cash via your broker, and BTC for when you want to move funds in the crypto ecosystem or deploy them into DeFi. A combo can also diversify regulatory risk – it’s unlikely both the ETF and direct Bitcoin would face issues simultaneously.

Cryptonews Tip: Ultimately, consider your goals and capabilities. If you’re purely investing and want it hassle-free, IBIT is tailored for you. If you aim to own and utilize Bitcoin truly, go for BTC. And there’s nothing wrong with doing a bit of each – many do, using IBIT for convenience in some accounts and holding BTC personally as an “insurance policy” against the traditional system.

Practical Guide: How to Buy IBIT or Bitcoin

By now, you should know which option (or combination) fits your needs. To conclude, here’s a brief step-by-step on actually purchasing IBIT vs buying Bitcoin directly, and what to do afterward in each case.

Buying IBIT (Bitcoin ETF)

- Open or use a brokerage account: To buy IBIT, you need a brokerage account that offers US stock trading. This could be an online platform like Fidelity, Charles Schwab, E*Trade, Robinhood, etc. If you already invest in stocks, you can likely buy IBIT there (ensure you have access to Nasdaq-listed securities – most do).

- Search for the ticker “IBIT”: In your brokerage’s trading interface, search for IBIT (iShares Bitcoin Trust ETF). Verify that it’s the BlackRock iShares Bitcoin Trust – by now, there may be a few other Bitcoin ETFs, but IBIT is the largest. Its profile should show it as a Digital Assets or Commodity ETF. Take note of the current price per share and perhaps the NAV if displayed.

- Place an order: Decide how many shares you want or how much money you want to allocate. You can place a market order (which will execute immediately at the current price) or a limit order (specify a price you’re willing to pay – valid if the market is volatile or if trading after-hours). Because IBIT can be somewhat volatile intraday (tracking BTC swings), limiting orders or trading during high-volume periods can be wise to avoid slippage.

- Execute and settle: You’ll see IBIT shares in your account once your order fills. Settlement is typically T+1 or T+2 (1-2 business days), like other ETFs, but your exposure starts immediately. From here, you can hold as long as desired. If needed, you can also sell IBIT just like a stock. Pro tip: Avoid trading near market close on Fridays if you’re concerned about weekend Bitcoin moves, as you can’t react until Monday.

- Store or utilize shares as needed: Your IBIT shares don’t require special storage – they sit in your brokerage. You might consider enabling features like dividend reinvestment (irrelevant here since no dividends) or margin if you plan to borrow against them. Review your broker’s fees; most don’t charge commissions for ETFs now. Keep an eye on IBIT’s premium/discount (usually minimal). That’s it – you’ve got Bitcoin exposure! Any gains or losses will appear in your account balance. Remember, for taxes, you’ll rely on the broker’s 1099 form later.

Buying Bitcoin (BTC) Directly

- Choose a crypto exchange or platform: Pick a reputable cryptocurrency exchange or brokerage to buy actual Bitcoin. Popular options in the US include Coinbase, Kraken, Binance.US, Gemini, Cash App, etc. Alternatively, some traditional fintech apps (PayPal, Robinhood) let you buy BTC, but not all allow you to withdraw to your wallet – ideally, choose one where you can withdraw your BTC. If decentralization is a priority, you might use a decentralized exchange or peer-to-peer marketplace (like Bisq or HodlHodl). Still, for beginners, a well-known centralized exchange is the simplest.

- Sign up and complete KYC: Most regulated crypto exchanges will require identity verification (providing ID, personal info) to comply with laws. Set up your account and secure it with two-factor authentication.

- Fund your account: Deposit fiat currency (USD, etc.) via bank transfer, ACH, debit card, or other methods the exchange supports. Some platforms also allow credit cards or PayPal, but watch out for fees. Depending on the method, funding might take a few minutes to a few days (ACH is typically quick).

- Place a buy order for Bitcoin: Navigate to the BTC/USD (or BTC/your currency) trading pair on the exchange. You can usually do a market buy (straightforward, but you’ll get the current market price) or a limit buy (set a price, for example, if you think BTC might dip and want to buy lower). Using a brokerage app like Cash App might be as simple as entering a dollar amount and hitting buy, without manual order types. Note the fees: an exchange might charge around 0.1% to 0.5% per trade, or a flat fee for small purchases.

- Obtain your Bitcoin in your exchange wallet: After execution, you’ll see your Bitcoin balance on the exchange. You technically own Bitcoin at this point, but it’s held by the exchange on your behalf. It’s highly recommended to move it to your wallet if it’s significant. Leaving it on an exchange means you’re trusting that platform (which introduces some counterparty risk, like IBIT, but without the regulatory protections).

- Set up a personal wallet: If you don’t already have one, choose a Bitcoin wallet. For serious investors, a hardware wallet (like Ledger Nano or Trezor) is the safest crypto wallet – purchase one from the manufacturer, initialize it securely (write down your recovery seed phrase), and connect it to the provided app. If you prefer software, there are mobile wallets (such as BlueWallet, Exodus) or desktop wallets. Ensure that whatever wallet you use gives you control of the seed phrase/private keys (custodial wallets are essentially like leaving at an exchange).

- Withdraw BTC to your wallet: From the exchange, withdraw your Bitcoin. You’ll need to paste your wallet’s Bitcoin address. Double-check that the address is correct (sending to the wrong address is irreversible!). Also, be mindful of network fees – the exchange will show the withdrawal fee; when the network is congested, fees can be higher. Withdrawals usually take 10 minutes to an hour to confirm on the blockchain (six confirmations are standard for finality).

- Secure your holdings: Once in your wallet, secure your backup. Store your seed phrase offline in a safe place (or multiple places). Enable any additional wallet security features. Now your Bitcoin is under your custody. You should periodically update the wallet software/firmware as recommended and consider best practices (such as multi-sig if you have a large amount, splitting coins among addresses, etc.).

From here, you can hold your Bitcoin as a long-term investment, just as you’d hold IBIT, but now with the ability to use it as you please. If you want to use your BTC, you can send some to others, experiment with Lightning (which may involve opening channels), or even trade it for other cryptos on decentralized platforms. Be aware of the tax implications of each move. You’d reverse the process when you want to sell Bitcoin for cash: send BTC from your wallet to an exchange, then sell it for USD and withdraw to your bank.

Buying Bitcoin directly has a few more steps than buying IBIT, but many find it straightforward after the first time. And once set up, you have the full spectrum of Bitcoin’s utility at your fingertips.

👉 Learn here if it’s too late to buy Bitcoin in 2026?

Final Thoughts: Align Your Choice With Your Goals

IBIT offers simplicity: Brokerage integration, regulatory protections, and outsourced security. You sacrifice control and pay 0.25% annual fees. Bitcoin provides sovereignty: Full self-custody, zero management fees, and access to innovations like Lightning. You handle security and complex reporting. IBIT fits traditional portfolios; BTC enables actual crypto utility.

Reflect on your priorities: Do you value control or convenience? Can you manage keys versus preferring SIPC insurance? Consider long-term costs (fees compound) versus access needs (DeFi/payments). Your technical comfort and investment goals – pure exposure versus ecosystem participation – determine the best fit.

Neither option is universally superior. Volatility affects both. This comparison informs your decision, but it isn’t financial advice. Research thoroughly and assess personal risk tolerance before investing in Bitcoin or IBIT.

👉 Learn more: 7 best crypto ETFs to invest in 2025

FAQs

How closely does IBIT track Bitcoin?

Will IBIT pay a dividend?

Can retail investors redeem IBIT shares for on-chain Bitcoin?

Can you use IBIT or Bitcoin as collateral for loans?

Is IBIT a good ETF for Bitcoin?

References

- iShares Bitcoin Trust ETF (iShares by BlackRock)

- Bitcoin Goes Mainstream: IBIT Volatility Drops to SPY Levels (ETF.com)

- IBIT to BTC Calculator (BiTBO)

- Securities Act of 1933 (Cornell Law School)

- What SIPC Protects (SIPC)

- Bitcoin – BTC (Coinbase)

- About Form 1099-B, Proceeds from Broker and Barter Exchange Transactions (IRS)

- Sales and Other Dispositions of Capital Assets (IRS)

2M+

250+

8

70

About Cryptonews

Our goal is to offer a comprehensive and objective perspective on the cryptocurrency market, enabling our readers to make informed decisions in this ever-changing landscape.

Our editorial team of more than 70 crypto professionals works to maintain the highest standards of journalism and ethics. We follow strict editorial guidelines to ensure the integrity and credibility of our content.

Whether you’re looking for breaking news, expert opinions, or market insights, Cryptonews has been your go-to destination for everything cryptocurrency since 2017.