IBIT vs FBTC: Fees, Performance & Which Bitcoin ETF to Buy

IBIT and FBTC are the top two U.S. spot Bitcoin ETFs, meaning they hold actual Bitcoin, not just futures. Both let you invest in Bitcoin through a traditional brokerage account, but there are key differences between IBIT and FBTC in fees, liquidity, and how they fit different investor goals.

In a nutshell, traders might favor IBIT for its huge volume and tiny spreads. In contrast, long-term investors (especially in retirement accounts) may lean toward FBTC for its integration with Fidelity’s ecosystem.

This guide will compare FBTC vs IBIT ETFs head-to-head on fees, performance, structure, and more, so you can decide which Bitcoin ETF is better suited for you.

IBIT vs FBTC: Key Stats Compared

Here’s a side-by-side look at the two largest U.S. spot Bitcoin ETFs, BlackRock’s IBIT and Fidelity’s FBTC. The table compares key stats like assets, fees, and structure to help you understand how they stack up.

| Name | iShares Bitcoin Trust ETF | Fidelity Wise Origin Bitcoin Fund (ETF) |

|---|---|---|

| Ticker | IBIT | FBTC |

| Issuer | BlackRock | Fidelity |

| Launch Date | Jan 2024 | Jan 2024 |

| AUM (November 2025) | $87.5 billion | $22 billion |

| Expense Ratio | 0.25% | 0.25% |

| Custodian | Coinbase (Coinbase Prime) | Fidelity Digital Assets |

| Avg. Spread | 0.02% | 0.04% |

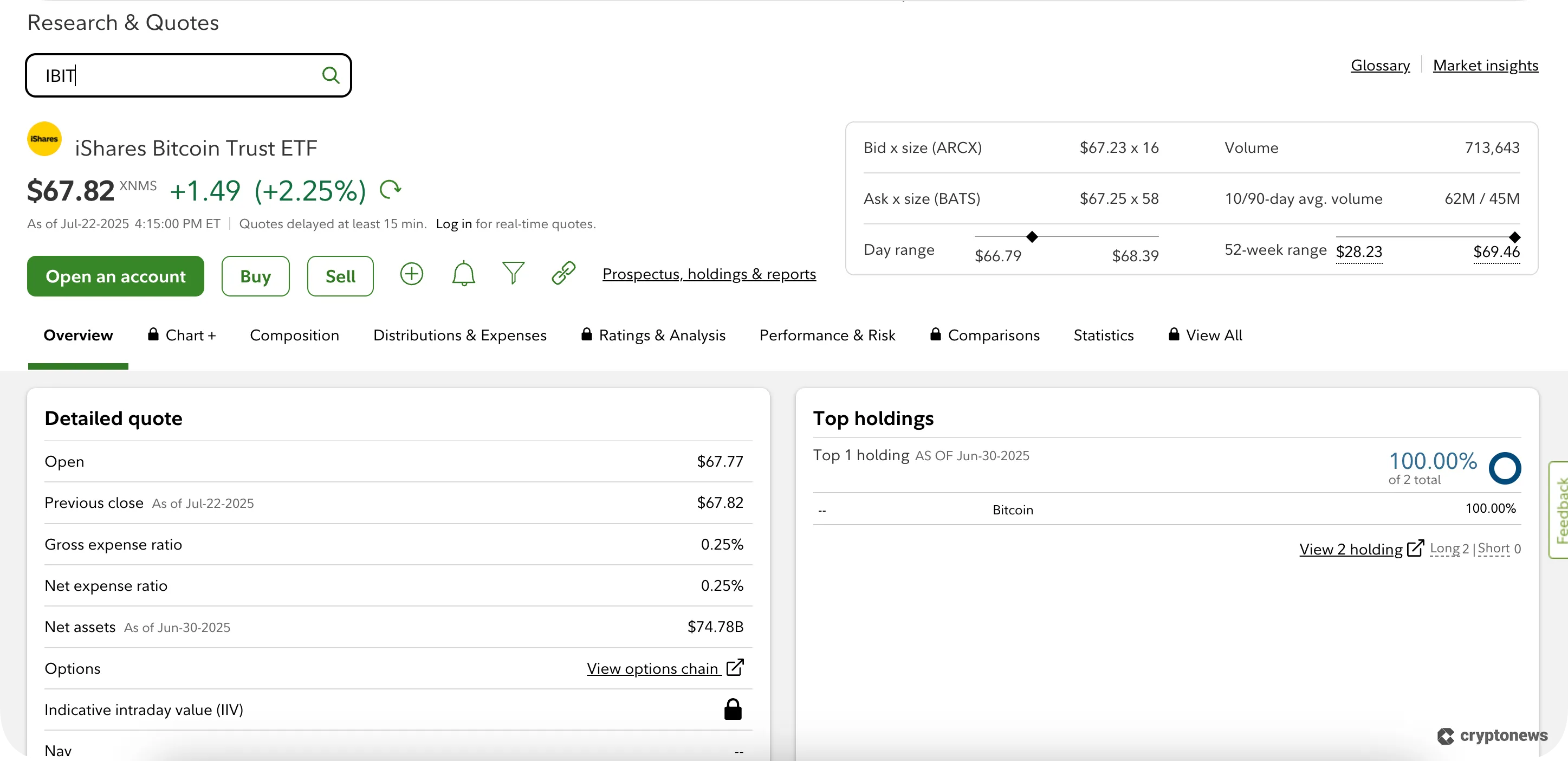

| Share Price | $36.23 | $55.62 |

| BTC per Share | 0.00057 BTC | 0.00087 BTC |

What Are IBIT and FBTC?

IBIT and FBTC are spot Bitcoin ETFs — funds that hold Bitcoin on investors’ behalf, rather than futures contracts. They mirror Bitcoin’s price and trade on stock exchanges like any ETF, allowing investors to get exposure to BTC without managing a crypto wallet.

These products were first approved in the U.S. in January 2024, opening the floodgates for mainstream Bitcoin investing.

Both IBIT and FBTC are structured as grantor trusts (not as traditional 1940-Act ETFs), but function similarly to ETFs in practice: you can buy and sell shares through any regular brokerage.

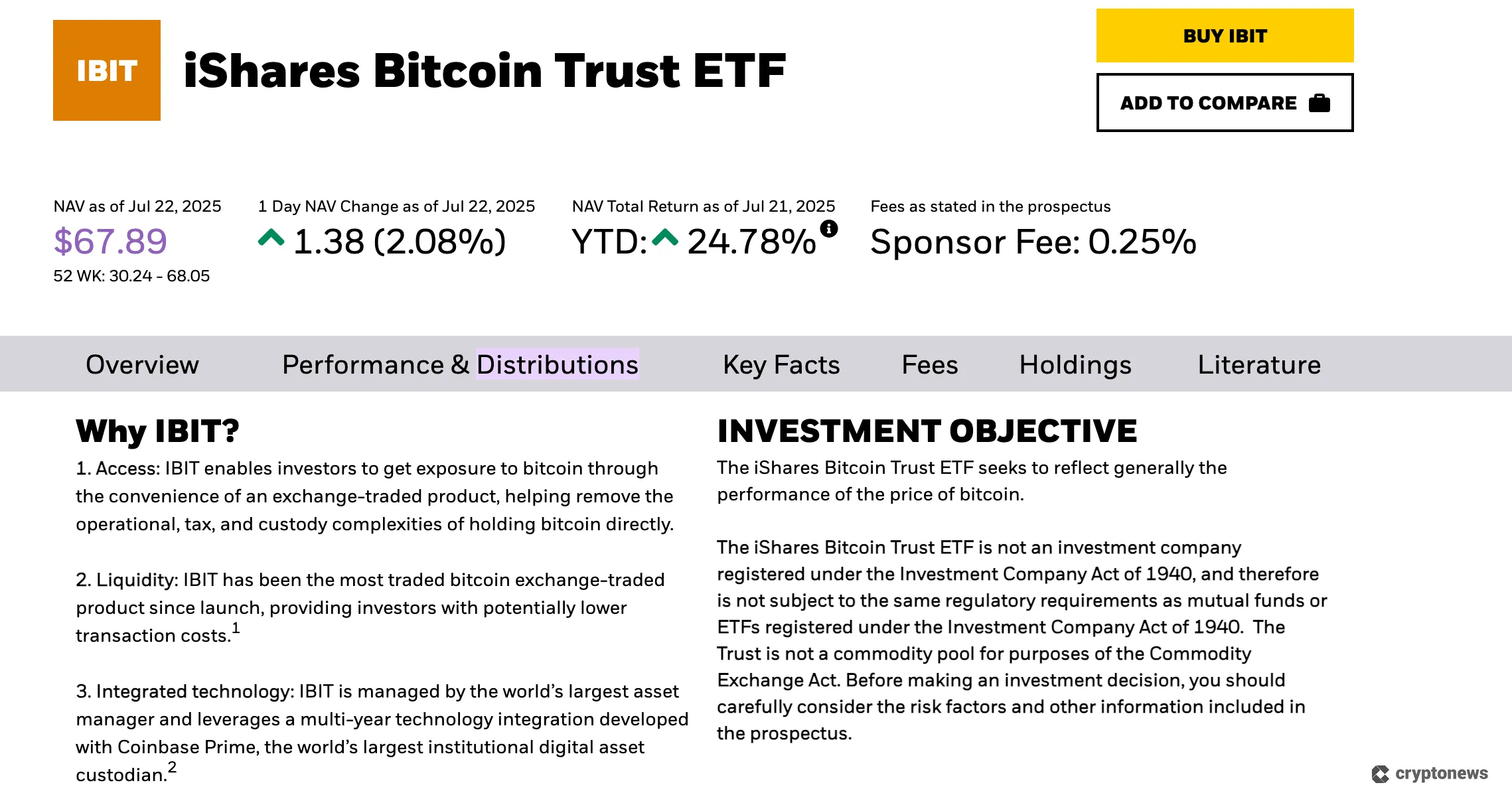

IBIT: BlackRock iShares Bitcoin Trust ETF

Launched by BlackRock’s iShares on January 11, 2024, IBIT quickly became the largest Bitcoin fund. It’s backed by the heft of BlackRock, the world’s largest asset manager, and integrates with Coinbase Prime for custody.

IBIT’s scale and liquidity are unparalleled: it gathered over $70 billion in assets within its first year and consistently leads in trading volume. This makes IBIT attractive to institutional traders and those who value deep liquidity.

👉 Don’t Miss: iShares Bitcoin Trust (IBIT) ETF Price Prediction 2026-2030

BlackRock structured IBIT with a relatively low share price (by using more shares per BTC held), which doesn’t affect performance but does make IBIT trade in smaller chunks, potentially convenient for fine-tuned trading.

Overall, IBIT currently dominates the space, holding about 793K BTC (~$87B AUM as of November 3, 2025). It continues to be the main trading vehicle, with big institutions piling in. For example, Harvard disclosed a $116M IBIT stake in August filings.

FBTC: Fidelity Wise Origin Bitcoin Fund

Launched by Fidelity on the same day (January 11, 2024), FBTC is Fidelity’s spot Bitcoin ETF offering. It holds actual Bitcoin with custody by Fidelity Digital Assets (Fidelity’s in-house crypto custody arm).

Fidelity aimed this product at financial advisors and long-term investors. It’s integrated into Fidelity’s brokerage and retirement platforms, meaning you can easily hold FBTC in Fidelity IRAs or other accounts.

Many crypto enthusiasts moved their retirement accounts to Fidelity specifically to access FBTC. In its first year, FBTC accumulated over $20 billion in Assets Under Management (AUM) — impressive, though still a fraction of IBIT’s size.

As of early November 2025, FBTC holds around 201K BTC, keeping it solidly in second place. However, flows have been more volatile. For example, August 19 saw $246M in redemptions, one of the fund’s largest single-day outflows.

👉 Don’t Miss: Fidelity Wise Origin Bitcoin Fund (FBTC) Price Prediction 2026-2030

Its selling points include Fidelity’s trusted name, potentially easier access for 401(k) or advisor-managed portfolios, and familiarity with Fidelity’s interface for retail investors.

Both IBIT and FBTC offer a regulated, convenient way to invest in Bitcoin without worrying about private keys or crypto exchanges. Next, we’ll compare their performance side by side.

IBIT vs FBTC: Performance Comparison

Regarding IBIT vs FBTC performance, the two funds have been neck and neck. Both aim to track spot BTC as closely as possible, and indeed, their returns since inception have been almost identical to each other and to Bitcoin itself.

Since Inception (Early 2024 to Mid-2025)

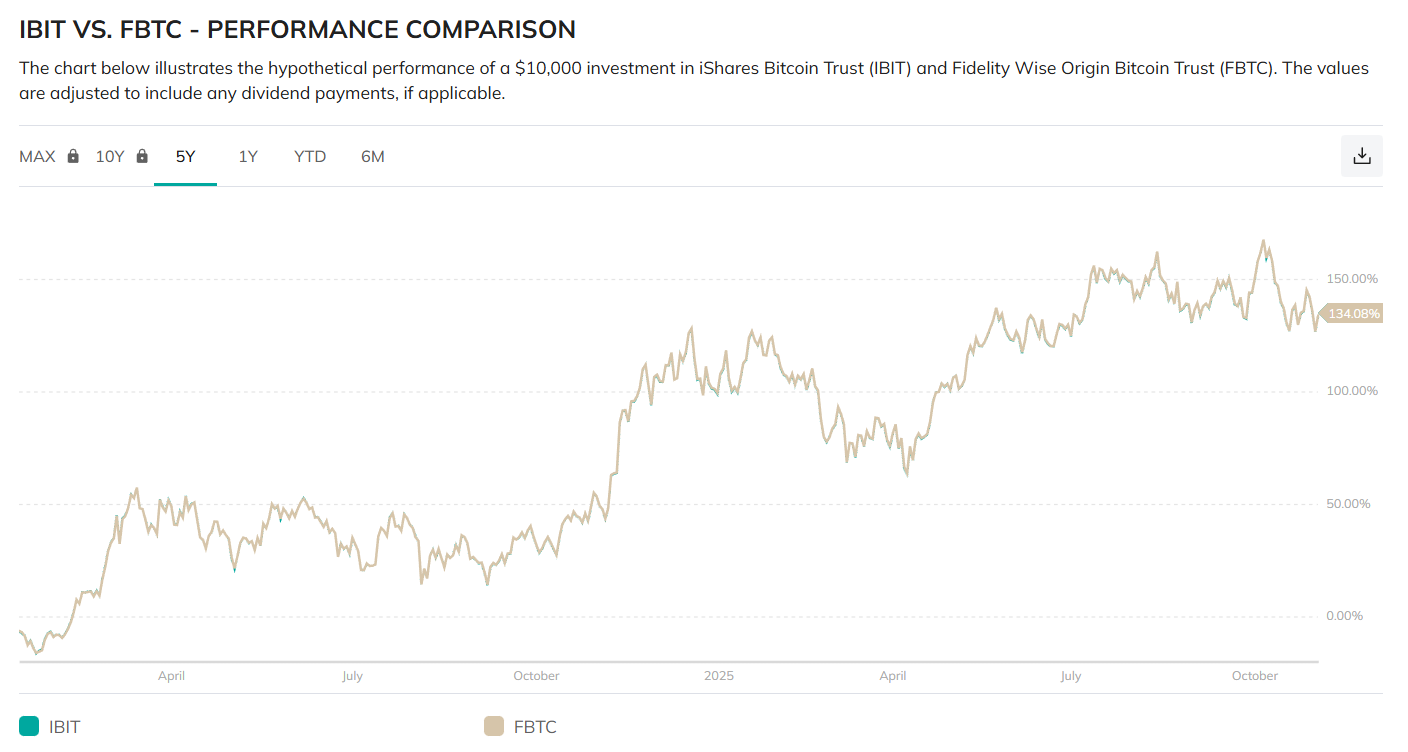

IBIT and FBTC delivered roughly 134% total return from launch through November 2025.

Essentially, a $10,000 investment on launch day would be worth over $23,500 by Q4 2025, reflecting Bitcoin’s price appreciation.

The tiny difference in IBIT vs FBTC performance (on the order of 0.1-0.3%) is due to minimal tracking error and fee effects.

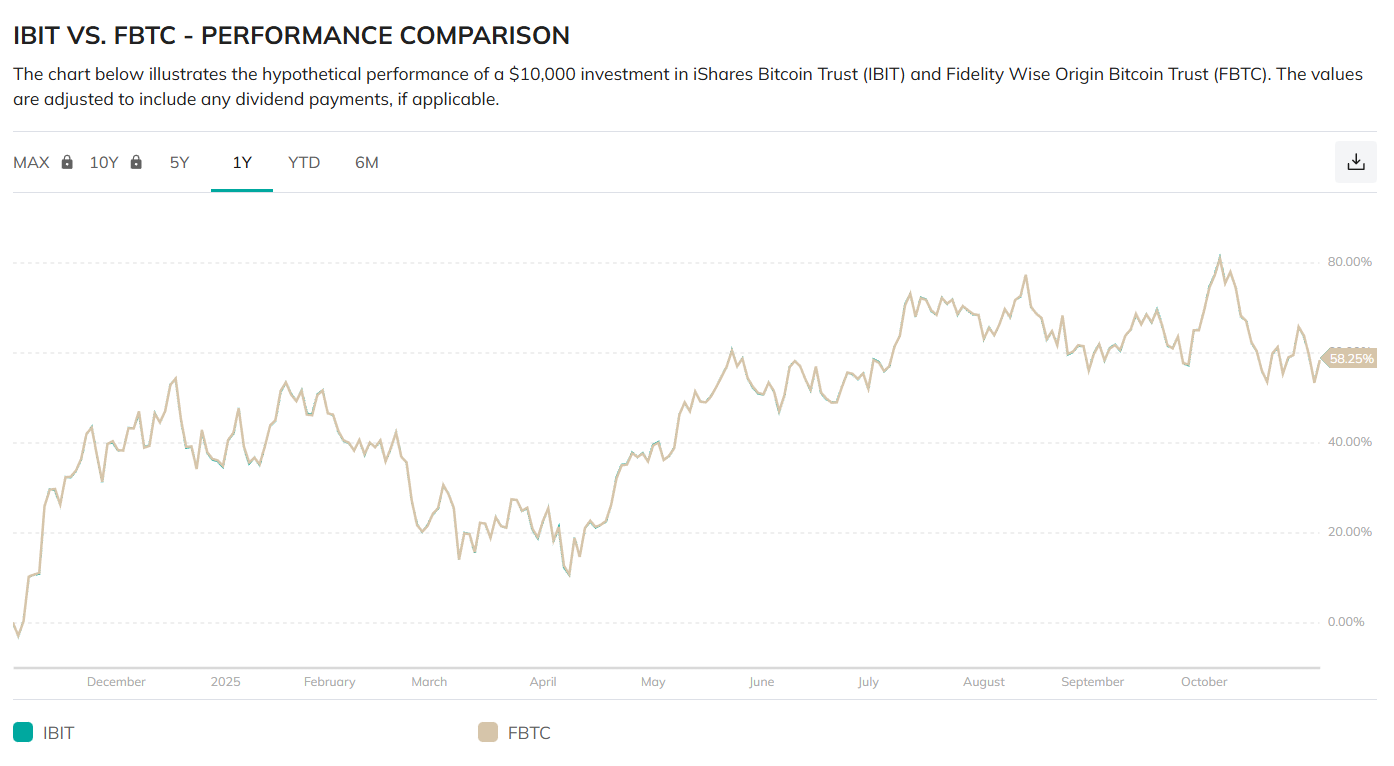

1-Year Recent Performance

Over the past year, FBTC and IBIT are up roughly 58% (as of Q4 2025), closely shadowing Bitcoin’s rise. Any given day or week, their price charts are virtually indistinguishable.

Neither fund has a notable performance edge; whenever Bitcoin rallies or dips, FBTC vs IBIT performance moves in tandem, usually within a fraction of each other.

Tracking Accuracy

Both ETFs have been very accurate in tracking the underlying BTC market. For example, since its inception, IBIT’s NAV total return has been 134.08% versus 134.38% for Bitcoin, with only a 0.3% lag. FBTC has a similarly tiny tracking error.

This is expected, as each charges a 0.25% annual fee, which only slightly drags performance. Minor timing differences (e.g., how daily NAV is calculated) and the cost of fund expenses explain the minuscule gaps.

Overall, tracking error has been negligible, a testament to efficient fund operations.

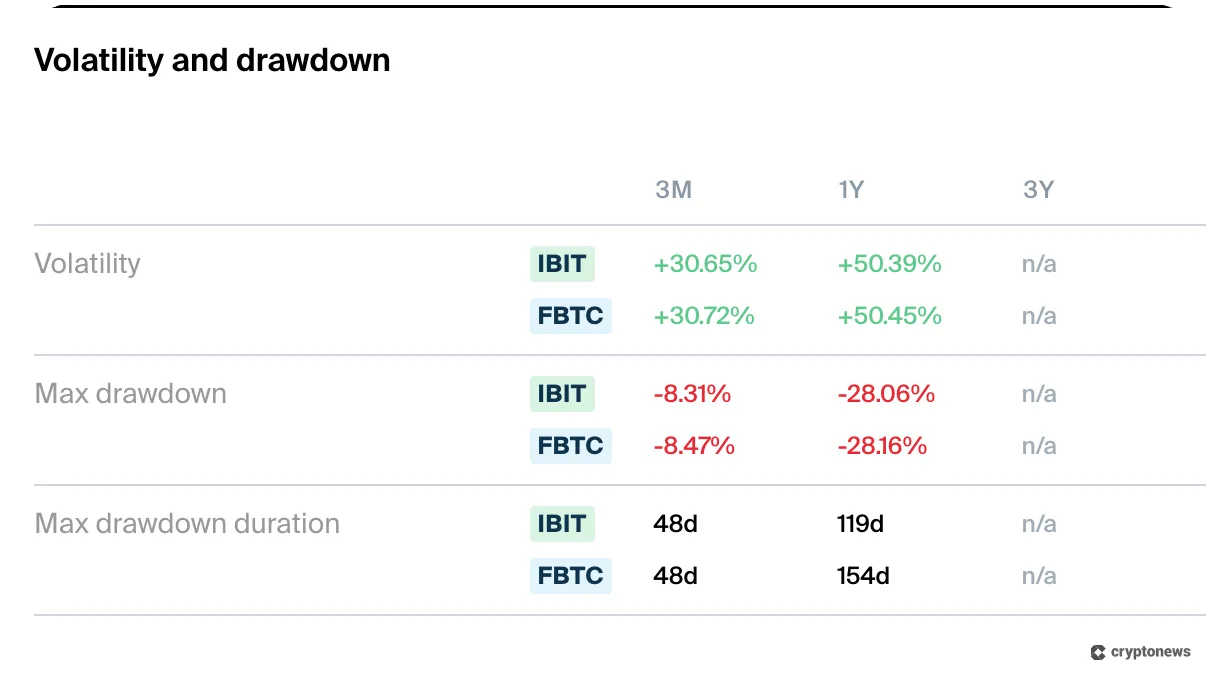

Volatility and Drawdowns

Since these funds track Bitcoin directly, expect big swings. While both are up over 134% since launch, they’ve had rough patches, too, like a 28% dip during spring 2024. They also show high volatility, with sharp price moves along the way.

In other words, they mirror Bitcoin’s ups and downs; neither fund is inherently more or less volatile.

Recent trading has underscored this volatility. Around August 14, when Bitcoin hit $124,000, IBIT took in nearly $500M of inflows, but just days later (August 20), it saw $218M in outflows as BTC retraced. FBTC similarly swung from inflows to large outflows.

⚖️ Final Verdict

IBIT and FBTC have identical performance. Neither has “alpha” — they are passive trackers of the same CME Bitcoin index.

You can expect both to rise and fall with Bitcoin’s price, minus a tiny fee. The charts for IBIT vs FBTC look like mirror images. The choice between them isn’t about return differences but fees, trading costs, and how they fit your use case.

Expense Ratios, Fees, and Costs

When it comes to fees, IBIT and FBTC are evenly matched. Both charge an annual expense ratio of 0.25%, meaning a $10,000 investment costs just $25 per year—a low fee by ETF standards, especially in crypto.

This single fee covers fund management, custody of the Bitcoin, and operational costs. Importantly, no hidden or performance-based fees exceed the stated 0.25%.

Let’s discuss how costs break down.

Fee Waivers (Now Expired)

Both funds launched with promotional waivers:

- IBIT (BlackRock): Waived fees on the first $5 billion in assets for the first 12 months.

- FBTC (Fidelity): Charged 0% on its first $1 billion for the first 6 months, through July 2024.

These promos helped attract early assets, but as of mid-2025, both funds charge the full 0.25%. They also trade commission-free on many platforms, including Fidelity’s own brokerage.

Trading Spreads

Beyond the official expense ratio, you should also consider the bid/ask spread — the difference between buying and selling prices. This affects what you pay when trading.

- IBIT has a slight edge in liquidity, with an average spread of just 0.02% (around a penny per share).

- FBTC typically sees a spread of 0.04%, still extremely tight.

For most long-term investors, these differences are negligible (just a few cents). But if you’re trading large volumes, IBIT’s deeper liquidity may lower transaction costs slightly.

Premiums and Discounts

Unlike older crypto funds, these ETFs trade very close to their net asset value (NAV).

- Deviations from NAV are usually under 0.2%, thanks to strong arbitrage activity.

- This means you’re paying a fair price for the underlying Bitcoin, with minimal distortion.

⚖️ Final Verdict

Cost isn’t a deciding factor between IBIT and FBTC. They’re both among the cheapest crypto ETFs available. Their 0.25% fee is far lower than the 1.5% fee charged by the legacy Grayscale Bitcoin Trust (GBTC).

If anything, IBIT’s massive size has driven industry-wide fee competition and gives it a slight liquidity advantage. But both funds are equally low-cost and efficient for long-term, buy-and-hold investors. Just keep an eye out as fee cuts could continue across the market.

Liquidity and Tradability

Liquidity is among the most significant practical differences between the IBIT and FBTC matchups. IBIT is a goliath in terms of trading activity. It regularly trades millions to billions of U.S. dollars daily in volume (often more than any other Bitcoin-linked asset).

FBTC also has healthy volume, typically in the hundreds of millions per day, but it hasn’t matched IBIT’s trading frenzy. On average, IBIT’s trading volume is several times higher than that of FBTC.

For example, in early 2025, IBIT saw over $2 billion in daily trading, whereas FBTC averaged under $0.5 billion. This gap has likely widened as IBIT’s AUM soared.

For Active Traders

If you move large orders, IBIT’s superior liquidity means tighter spreads (around 0.02%) and massive capacity. A high-volume trader will find getting in and out of IBIT easier without moving the price.

Given the deep order books, slippage is minimal even for big trades. FBTC, while plenty liquid for most retail needs, has less activity. Its bid-ask spread around 0.04% is still very low, but IBIT may execute large orders slightly more efficiently in fast markets.

In short, day traders or those frequently rebalancing positions might prefer IBIT for its extra liquidity cushion. IBIT has essentially become the “mega-cap” Bitcoin fund that institutions trade in and out of heavily, akin to how SPY (S&P 500 ETF) dominates stock ETF trading.

For Institutions

Large institutional investors have gravitated toward IBIT for the same liquidity reasons. BlackRock’s product quickly attracted hedge funds, ETFs-of-ETFs, and other big players; its creation/redemption mechanisms are very robust, keeping volumes high.

Options activity also reflects IBIT’s dominance. In mid-August, put options on IBIT traded at their widest premium to calls since April, showing institutions actively hedging downside exposure in the ETF rather than in FBTC.

That said, FBTC is no slouch. It also sees millions of shares traded daily and has tight markets.

Institutions concerned with custody risk might prefer FBTC’s self-custody approach despite the slightly lower liquidity. But generally, IBIT has become the primary trading vehicle for U.S. spot Bitcoin exposure, with FBTC as a strong secondary option.

For Long-Term Investors

Liquidity is less critical day-to-day if you’re just buying and holding. Both funds are liquid enough to buy into or cash out without trouble.

Even FBTC’s $300-400 million daily volume is plenty for retail investors. Avoid trading off-peak hours and consider using limit orders to get optimal pricing.

💡 One thing to note: Some brokerage platforms (especially early on) made one fund easier to access than the other.

For instance, Vanguard initially restricted crypto ETFs, prompting some investors to move IRAs to Fidelity to buy FBTC. Meanwhile, IBIT’s being on NASDAQ ensured it was broadly available. Most brokers allow both by now, but check your brokerage’s policy.

⚖️ Final Verdict

IBIT is the liquid of the two ETFs, benefiting active traders and large investors. FBTC is also plenty liquid for typical investing and has decent trading spreads, just slightly wider than IBIT’s.

Unless you’re executing very large trades or rapid-fire strategies, FBTC’s liquidity is likely sufficient. But if you want the absolute highest trading volume and lowest spreads in the Bitcoin ETF space, IBIT leads the pack.

Security, Structure, and Custody

Though we call them ETFs, IBIT and FBTC are legally structured as grantor trusts (similar to the SPDR Gold Trust or Grayscale’s BTC trust) and are not regulated under the Investment Company Act of 1940.

This structure was how the SEC allowed a spot Bitcoin “ETF” — technically, it’s a trust that holds Bitcoin and issues shares. For investors, the experience is essentially the same as an ETF.

🔑 One key point: As trusts, they do not use leverage or crypto derivatives — they hold actual Bitcoin 1:1, and the trust’s value directly reflects the Bitcoin price. There’s no internal lending or staking of the assets, which keeps things simple and transparent.

Custody

➡️ BlackRock chose to outsource custody to Coinbase. Coinbase Prime is the crypto custodian holding Bitcoin for IBIT. BlackRock already partnered with Coinbase (connecting its Aladdin platform to Coinbase in 2022), so they leveraged Coinbase’s established institutional custody capabilities.

Coinbase holds the private keys and is responsible for securing IBIT’s hefty Bitcoin stash (over 790K BTC by Q4 2025). Coinbase has extensive crypto-specific security expertise, but the downside is that it introduces a third-party risk.

If Coinbase had an issue, IBIT could be affected. Some crypto purists note this as a single point of failure. BlackRock, of course, did due diligence, and Coinbase is a regulated NYDFS custodian, but the risk is worth mentioning.

➡️ Fidelity self-custodies Bitcoin via its Fidelity Digital Assets subsidiary. It holds the private keys in-house using an “omnibus storage,” which blends hot and cold storage for security and liquidity.

Fidelity has been involved in Bitcoin since 2014 and has built its custody tech, so it uses that experience here. It keeps complete control, with no reliance on an outside exchange for custody. Many investors trust Fidelity’s brand and security track record.

With FBTC, your Bitcoin is held by a 75-year-old financial institution (Fidelity) that has heavily invested in crypto security. This can reassure long-term investors who are concerned about third-party exchange failures (especially after seeing events like FTX’s collapse).

Security

Both funds employ state-of-the-art security practices: Multi-signature wallets, air-gapped cold storage, audits, and more. BlackRock and Fidelity understand that any security breach would be catastrophic, so they’ve spared no expense.

Coinbase’s custody has insurance coverage and a $120M crime policy (as of launch), and Fidelity Digital Assets is regulated in New York and similarly insured.

From an investor standpoint, IBIT and FBTC are far more secure than managing your private keys if you’re not experienced. They eliminate the risk of losing a hardware wallet or being hacked individually.

However, they introduce institutional risk (you trust Coinbase or Fidelity not to get hacked). The good news is that both custodians have a clean security track record.

Trust Structure and Tax

As grantor trusts, IBIT and FBTC do not produce K-1 forms (they are not partnerships). Instead, you’ll get a Form 1099-B or similar tax document, and you’re taxed as if you directly held your proportionate share of Bitcoin. Any gains you realize by selling shares are taxed as capital gains (like stocks or ETFs).

There are no capital gains distributions or interest distributions to worry about each year; any taxable events only occur if you sell shares, or potentially a tiny amount if the fund sells a bit of BTC to pay the expense ratio.

(Both trusts periodically sell small amounts of Bitcoin to cover the 0.25% fee, which technically means shareholders have a small taxable gain distributed, but it’s minimal.)

The bottom line is that crypto tax treatment is straightforward: No pass-through of complicated income, no K-1s, just 1099 proceeds reporting. Of course, these concerns are moot in an IRA or 401(k).

⚖️ Final Verdict

Both IBIT and FBTC have robust security and custody setups. The main difference is that Coinbase and Fidelity hold the keys.

They share a similar trust structure, providing transparency and relatively simple taxes (especially compared to futures-based funds). Neither fund lends out Bitcoin, so you don’t get yield, but also avoid the counterparty risks of lending.

Do IBIT and FBTC Pay Distributions?

No, neither IBIT nor FBTC pays any distributions (dividends or interest). These funds hold only Bitcoin, which is a non-income-producing asset. Bitcoin doesn’t generate interest or dividends, so there’s nothing to distribute.

If you’re an investor who needs income or yield, a spot Bitcoin ETF will not provide it. Your “gain” is simply if the price of BTC goes up. If you want to realize profit, you’d have to sell shares.

This contrasts with other ETFs that might pay distributions (for example, certain commodities funds that hold Treasury bills as collateral, or futures-based ETFs that distribute roll yield or interest).

The fund sponsors have confirmed no intent to lend out the bitcoin for income (which aligns with the SEC’s requirements for approval).

If you prefer an investment that produces income, you’d have to look at other areas. For example, some blockchain stocks pay dividends, or you could consider covered-call strategies on these ETFs to generate income, albeit with trade-offs. But IBIT/FBTC themselves won’t give any yield.

How Much IBIT or FBTC Equals One Bitcoin?

Because each share represents only a fraction of a Bitcoin, you might ask: How many shares make one BTC? The conversion can be found from the trust’s holdings.

As of mid-2025:

- IBIT: Holds around 793,000 BTC and has approximately 1.33 billion shares outstanding. This comes out to roughly 0.00057 BTC per share. Invert that, and about 1,820 IBIT shares ≈ 1 Bitcoin.

- FBTC: Holds around 201,000 BTC with approximately 234 million shares (estimated) outstanding. That’s about 0.00087 BTC per share, meaning ~1,136 FBTC shares ≈ 1 Bitcoin.

Fund companies periodically publish the exact “BTC per share” on their websites. For example, on November 3, 2025, one FBTC share corresponded to about 0.000874 BTC and one IBIT share to about 0.000570 BTC (hence the price difference, as noted).

Why does this ratio change?

This is primarily due to the expense ratio. The funds sell a bit of Bitcoin daily to pay the 0.25% annual fee. That gradually reduces the BTC backing each share. The reduction is minimal (0.25% per year would mean about 0.000882 → 0.000880 over a few weeks).

However, over many years, if Bitcoin’s price stayed flat, the share price would slowly drop relative to BTC due to fees. As Bitcoin’s price changes swamp the tiny fee effect, you won’t notice this much in a rising market.

For practical purposes, you can always find the current BTC-per-share on the sponsor’s site or calculate it using the formula:

It varies a bit from day to day. But knowing this is useful: If you ever want the equivalent of 0.5 BTC, you can calculate how many shares to buy.

To illustrate, imagine Bitcoin is $120,000:

- IBIT share ≈ $66, so ~1,818 IBIT shares ~ $120,000 (about one BTC worth).

- FBTC share ≈ $105, so ~1,143 FBTC shares ~ $120,000 (one BTC worth).

If BTC hits, say, $200,000, you’d see IBIT around $110/share and FBTC around $176/share, meaning you’d need more IBIT shares to equal one BTC.

It’s just a unit difference. So don’t be thrown off by the share price differences. Focus on how much Bitcoin exposure you want and buy the number of shares corresponding to that.

IBIT and FBTC Use Cases: Which ETF Is Right for You?

Now that we’ve covered stats and mechanics, let’s discuss which Bitcoin ETF fits your needs. Both funds give you Bitcoin exposure, but certain features might make one a better choice depending on your investment context.

Below, we break down some common investor types and how FBTC vs IBIT might stack up:

Long-Term Retirement Investors

If you plan to hold Bitcoin in a 401(k) or IRA for the long haul, FBTC is a strong option, especially if you already use Fidelity. It fits smoothly into traditional retirement accounts like Roth or Traditional IRAs and could offer tax-deferred or even tax-free growth, depending on your account type.

Fidelity was among the first to support Bitcoin in 401(k)s (with employer approval), and FBTC was built with retirement portfolios in mind. Some investors have even switched their IRAs to Fidelity just to access it. While IBIT is also IRA-eligible at many brokers, FBTC is often easier if you’re already in Fidelity’s ecosystem.

Small differences in share price or liquidity don’t matter much for long-term holders. What tends to matter more is trust, integration, and ease of use. With Fidelity handling custody in-house, FBTC offers a reassuring setup, ideal for retirement savers who want to “set it and forget it” like they would with any core index fund.

High-Volume Traders

If you trade frequently, whether intraday, swing trading, or through other strategies, IBIT is the go-to Bitcoin ETF. It has the highest trading volume and tightest spreads in the space, which means better fills and lower slippage.

You can move large amounts without disrupting the market, making it ideal for active crypto trading strategies.

IBIT also leads in options activity, offering a growing market for strategies like hedging and covered calls. While FBTC has options too, IBIT’s are more liquid, giving traders more flexibility.

Its lower share price helps with fine-tuning positions and scaling in or out with precision. Plus, for algo trading or stop orders, IBIT’s deep order book offers extra stability during fast price moves.

IBIT is built for speed, volume, and execution. If you’re trading, it’s likely your best bet. Just be sure to use limit orders and stay alert — Bitcoin ETFs can swing fast.

Fee-Focused Buy-and-Holders

If keeping costs low is your top priority, both IBIT and FBTC are solid picks. They currently charge the same low expense ratio of 0.25%, and past fee waivers have ended, so it’s an even playing field now.

That said, there are a few small differences to keep in mind. IBIT’s massive scale could lead to future fee cuts, as BlackRock has shown it’s willing to compete aggressively on pricing. While that’s speculative, it’s something to watch if you’re in this for the long haul.

For those doing dollar-cost averaging, IBIT’s slightly tighter trading spreads might save you a bit over time. It’s not a game-changer, but every little bit helps.

Double-check your brokerage’s fee structure. Most treat both ETFs like any other stock or fund, but access to fractional shares or commission-free trades might vary slightly depending on your platform.

In the end, you won’t see a meaningful difference in costs between the two over a long time horizon. Both are efficient, low-cost ways to get Bitcoin exposure and are equally well-suited for a buy-and-hold approach.

Long-Term Outlook for IBIT and FBTC

What does the future hold for these Bitcoin ETFs? In the long run, the performance of IBIT and FBTC will be entirely driven by Bitcoin’s price trajectory. Neither fund is actively managed; it doesn’t try to beat the market; it is the market (for Bitcoin).

So your 10-year outcome investing in IBIT or FBTC is: How high (or low) will Bitcoin be 10 years from now?

📈 If Bitcoin Continues to Rise

Many crypto enthusiasts are bullish long-term. Let’s say Bitcoin reaches new heights like $150,000, $250,000, or even over $500,000 in the coming years. Under such scenarios, both IBIT and FBTC would increase in value proportionally.

- They will closely track any appreciation in BTC. For instance, if BTC hits $250k (roughly double the July 2025 price), IBIT shares would likely be over $140 and FBTC shares around $220.

- If Bitcoin 5xes to $500k (a more dramatic scenario), IBIT might be in the $300-$350 range, FBTC in the $520-$550 range, etc.

Essentially, expect whatever percent increase Bitcoin achieves, minus maybe around 0.25% per year in fee drag, to be reflected in your ETF shares.

📉 If Bitcoin Stagnates or Falls

Conversely, if Bitcoin’s price languishes or declines over the long term, IBIT and FBTC will also mirror that.

- A drop back to, say, $50k BTC (roughly half of mid-2025 levels) would cut these ETF prices roughly in half.

- In a prolonged flat period (imagine BTC stays around the same price for years), the only difference is that the small fee would slowly chip away at NAV (the funds would be selling a bit of BTC to pay expenses).

For example, if Bitcoin stayed at $100k for 10 years straight (hypothetically), you’d see IBIT/FBTC gradually drift down maybe around 2.5% total over that decade due to fees (0.25% × 10 years), all else equal.

So in a flat scenario, you slightly underperform holding actual bitcoin, but very slightly. In a down scenario, you lose value just as holding BTC outright would.

👪 Investor Adoption and AUM Growth

One interesting possibility, though it doesn’t directly change your returns, is that the growth of these funds might influence Bitcoin’s market. We’ve seen massive inflows; together, they hold over 940,000 BTC as of mid-2025 (about 4.5% of all Bitcoins).

If the adoption of Bitcoin ETFs keeps surging (perhaps spurred by more financial advisors allocating a portion of portfolios to BTC), buying pressure could be a tailwind for Bitcoin’s price.

Some analysts believe broader ETF adoption could push BTC to new highs, benefiting ETF holders. This is a bit reflexive; the more popular IBIT/FBTC gets, the more BTC they have to buy, potentially driving the price up and attracting more investors.

🧭 Competition and Changes

Over the next decade, we’ll likely see more Bitcoin and Ethereum ETFs, and possibly other crypto ETFs (several are already filed for approval).

IBIT and FBTC are currently dominant, but if another fund offers an ultra-low fee or some novel feature (like insurance or maybe allowing redemptions in Bitcoin), that could challenge them.

So far, though, IBIT and FBTC have the first-mover advantage and brand trust. They’ll probably remain top choices unless someone like Vanguard launches an even cheaper fund (purely hypothetical).

Keep an eye on fee reductions; a price war could happen if growth plateaus.

How Much Will IBIT Be Worth in 10 Years?

Nobody knows exactly where Bitcoin will be in 2035, but we can explore a few scenarios to get a sense of what IBIT might be worth based on different price outcomes.

If Bitcoin falls to $30,000, IBIT might drop to around $16.50 per share — a major loss. Even if Bitcoin stays flat near $120,000, IBIT could drift slightly lower over time due to fees. That’s the risk of long-term exposure.

If Bitcoin reaches $250,000, a single IBIT share (which holds about 0.00055 BTC) would be worth around $137. That’s roughly double today’s price, translating to steady growth, around 11% annually. Solid, but not explosive.

If Bitcoin skyrockets to $500,000 or even $1 million, IBIT could be worth $275 to $550 per share. That’s an 8–15x return, meaning a $10,000 investment could grow to $80,000–$150,000. Depending on macroeconomic factors and other variables, these outcomes are possible.

Note that if IBIT’s price climbs too high, BlackRock could do a share split to keep it more affordable to trade. This wouldn’t affect your investment value; it just changes the number of shares you hold. FBTC could do the same.

How Much Will FBTC Be Worth in 10 Years?

FBTC holds slightly more Bitcoin per share than IBIT, so its price will always be higher in dollar terms, but the percentage change will mirror Bitcoin’s performance.

Let’s look at a few possible futures:

If Bitcoin drops to $30,000, FBTC could fall to about $26.40 per share. Even if BTC stays flat near $120,000, FBTC might settle around $95–$100 due to long-term fee drag. These are the downside risks that come with crypto exposure.

If Bitcoin climbs to $250,000, FBTC would be worth about $220 per share (0.00088 × $250k). That’s roughly double its current price — a steady, long-term gain that reflects BTC’s projected growth.

At $1 million per Bitcoin, FBTC could reach around $880 per share. That’s an 8–10x return or more. A $10,000 investment could grow to $100,000+ if Bitcoin fulfills a long-term bull thesis.

One strategic benefit is that FBTC fits well inside retirement accounts like a Roth IRA. If Bitcoin reaches big numbers, selling FBTC tax-free could be a game-changer. Of course, this also applies to IBIT or any Bitcoin ETF in a tax-advantaged wrapper.

As always, Bitcoin’s path is uncertain. Regulatory changes, market evolution, or new custody solutions could reshape things over the next decade.

How to Buy IBIT or FBTC

Ready to add one of these Bitcoin ETFs to your portfolio? Buying IBIT or FBTC is straightforward, like purchasing any stock or ETF. Here are the steps.

Step 1: Choose a Brokerage

Ensure you have a brokerage account that offers access to U.S. stock exchanges. IBIT trades on the NASDAQ, and FBTC trades on Cboe BZX (but many brokerages will treat it like any other listed ETF). Major brokers like Fidelity, Schwab, E*Trade, TD Ameritrade, Robinhood, etc. provide access.

If your broker has restrictions on cryptocurrency-related securities (as Vanguard did initially), you may need to switch to one that doesn’t.

For instance, Fidelity, being the sponsor of FBTC, obviously supports it. In fact, Fidelity also lets you trade all iShares ETFs (including IBIT) commission-free.

Step 2: Search the Ticker

In your brokerage account, search for “IBIT” (for the BlackRock iShares Bitcoin Trust ETF) or “FBTC” (for the Fidelity Wise Origin Bitcoin fund). Ensure you got the correct symbol.

There are a few similarly named products internationally, but those tickers are correct for the U.S. spot ETFs. Just like any stock, you should see a quote showing the price.

Step 3: Place an Order

Decide how many shares you want to buy. You can enter a market order (which will execute immediately at the best available price) or a limit order (where you specify the maximum price you’re willing to pay, or the minimum price if selling).

Given the high liquidity and tight spreads, a market order during regular hours will usually fill near the quote. However, to be safe, many suggest using limit orders, especially if you’re trading a large quantity or trading outside of peak hours.

Step 4: Settlement and Holding

After execution, the ETF shares will appear in your account. From there, holding IBIT or FBTC is just like keeping any other stock/ETF. You can watch their price, set up alerts, or add them to your portfolio tracker.

If you’re buying in a tax-advantaged account (like an IRA), you won’t have immediate tax implications. If buying in a taxable account, note your cost basis for future capital gains/loss calculations.

Availability in IRAs/401(k)

As mentioned, you can hold these in retirement accounts. If you use Fidelity for your IRA, you can directly purchase FBTC or IBIT in the IRA (Fidelity even classifies them under “Crypto” in the stock screener). Other IRA custodians should allow it too, since it’s a listed security.

For 401(k) plans, it’s trickier; only some plans offer a brokerage window or specific inclusion of these ETFs. If your 401(k) doesn’t, you might use an IRA rollover or invest in a taxable account.

But it’s worth checking if your employer’s plan, administered by Fidelity, for example, might allow a portion into FBTC as an alternative asset.

Final Verdict on IBIT vs FBTC

IBIT and FBTC offer Bitcoin exposure at 0.25% fees — the cost is equal. But IBIT trades more easily with tighter spreads, which is ideal for active moves.

Ultimately, the right ETF depends on how you invest. FBTC is a natural fit if you’re already with Fidelity, especially for long-term retirement accounts. On the other hand, if you trade frequently or use a different brokerage, IBIT’s higher liquidity and tighter spreads make it ideal.

Think about your timeline and comfort with risk. If you’re holding for years, FBTC’s seamless integration and trusted custody might give peace of mind. If you’re more active, IBIT’s trading efficiency can really matter.

Whichever you choose, check in regularly. Once a quarter, take a moment to review: Is the ETF tracking Bitcoin accurately? Have fees changed? Are new options available? The crypto landscape evolves quickly, and a quick review keeps your plan on track.

👉 Learn More: How to Get Into Crypto: A Complete Guide for Beginners

FAQs

What is the difference between FBTC and IBIT?

Is buying IBIT the same as buying Bitcoin?

Why is IBIT cheaper than FBTC?

Is IBIT a good ETF to buy?

Are FBTC and IBIT options cash settled?

How do IBIT and FBTC impact Bitcoin’s market price or liquidity?

Can you hold IBIT or FBTC in a Roth IRA or 401(k)?

Do IBIT or FBTC offer staking, lending, or yield features?

Are there international equivalents to IBIT and FBTC for non-U.S. investors?

References

- US Bitcoin ETF Tracker & AUM (Bitbo)

- Fidelity Investments® Launches Spot Bitcoin Exchange-Traded Product, Fidelity® Wise Origin® Bitcoin Fund (FBTC) (Fidelity)

- iShares Bitcoin Trust ETF (iShares)

- Laws and Rules (SEC)

- About Form 1099-B, Proceeds from Broker and Barter Exchange Transactions (IRS)

- Types of retirement plans (IRS)

- Harvard Reports $116M Stake in BlackRock’s iShares Bitcoin ETF in Latest Filing (CoinDesk)

- Blackrock (IBIT) iShares Bitcoin Trust Bitcoin Holdings (BitBO)

- Bitcoin ETF Net Daily Inflows & Outflows (BitBO)

- Insurance Against Price Slides in BlackRock’s Bitcoin ETF Now Costliest Since April Crash (CoinDesk)

- Bitcoin Hits $124K Record as 4 Tailwinds Align: Crypto Daybook Americas (CoinDesk)

2M+

250+

8

70

About Cryptonews

Our goal is to offer a comprehensive and objective perspective on the cryptocurrency market, enabling our readers to make informed decisions in this ever-changing landscape.

Our editorial team of more than 70 crypto professionals works to maintain the highest standards of journalism and ethics. We follow strict editorial guidelines to ensure the integrity and credibility of our content.

Whether you’re looking for breaking news, expert opinions, or market insights, Cryptonews has been your go-to destination for everything cryptocurrency since 2017.