Coinbase Overview

Key facts

Additional details

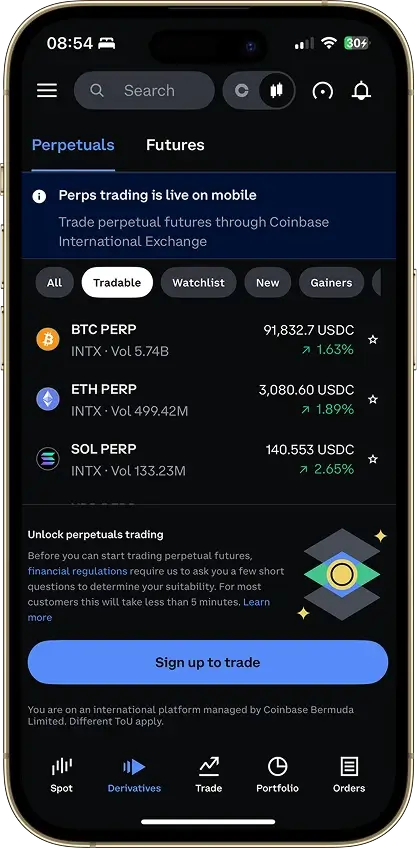

Coinbase Screenshots

Coinbase Pros and Cons

Pros

- SEC filings show more than a Merkle-tree snapshot

- Native USDC with near-free withdrawals on Base

- Free ACH and instant RTP cash-out

- Among the largest US spot venues

- Clean tax exports and CoinTracker link

Cons

- Simple buy carries a heavy spread

- Support is slow without Coinbase One

- Account locks are a recurring complaint

- New-fund staking paused in 4 states

Quick Decision: Is Coinbase Worth It?

Coinbase is worth considering if you want the safest regulated home for crypto in the US, can accept a high cost on the simple-buy screen, and plan to trade on Advanced Trade or hold a Coinbase One subscription. Its security record, public-company financials, and fast US cash-out are the reasons most people stay on the platform once they've found the cheaper screen.

It's a weaker fit for users who need the lowest fee on every buy, want fast human support without paying for it, or expect to stake in California, New Jersey, Wisconsin, or Maryland, where new-fund staking is paused. Use Coinbase if trust and clean records matter more to you than shaving fractions off every trade. Skip it if you trade often and refuse to touch the advanced interface.

Who Coinbase Is Best For And Who Should Skip It

Fit here comes down to user type rather than a claim that Coinbase works for everyone. The exchange is excellent for some traders and a costly choice for anyone who lives on the simple-buy screen, so it helps to see where you land before signing up. We compared other beginner-friendly crypto exchanges, and Coinbase consistently wins on trust signals even when it loses on price.

Coinbase fits naturally for a US resident who treats crypto as a long-term holding and wants the exchange itself to be the least risky part of the trade. The friction becomes too much for a high-frequency trader who lives on the simple-buy screen, where the spread quietly outweighs every other feature.

Features And Services

Coinbase is a full product ecosystem rather than a single app, and what a user can actually do spans a beginner buy screen, a professional trading interface, a self-custody wallet, a debit card, and a regulated derivatives venue. The catch is that these sit at very different price and risk levels, and the cheap, capable parts aren't the ones a new user lands on first.

The surface that decides the verdict is the split between simple buy and Advanced Trade. They run on the same balance, so the cost difference is a choice the user makes rather than a limit the platform imposes.

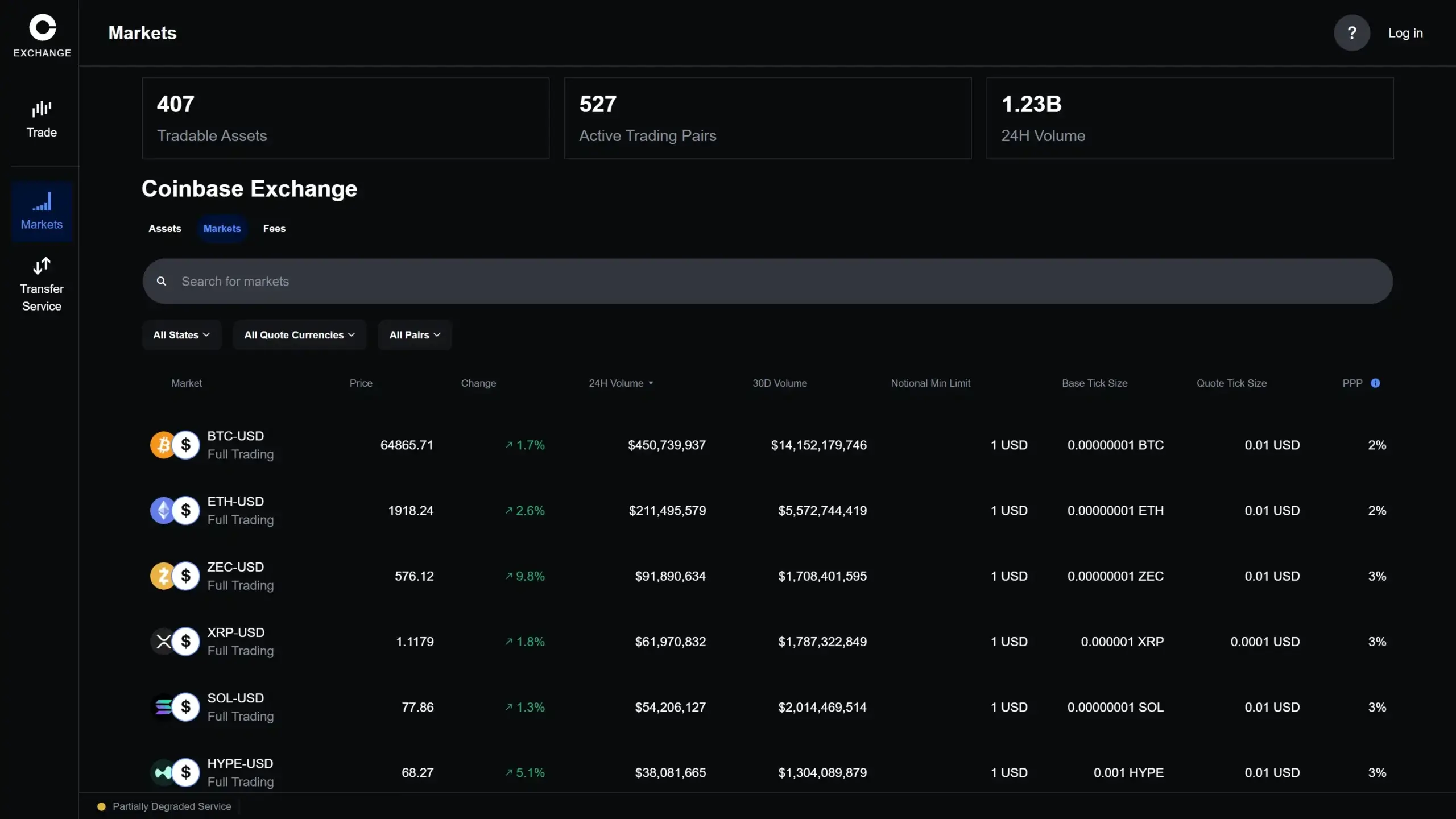

Supported Assets And Markets

Judge what you can actually trade and withdraw rather than the headline count. Coinbase lists roughly 270 to 315 assets and around 460 pairs for US retail, with native USDC and the major networks covered. That's a mid-size list, and it's deliberately narrower than offshore exchanges because Coinbase screens listings against US rules.

Coinbase covers the coins most US users actually buy and skips the long tail of low-liquidity tokens that offshore venues use to pad their numbers.

Staking And Rewards

Treat staking as a product decision rather than a free extra. Coinbase offers staking on major proof-of-stake assets and routes rewards through the app, but the value depends on commission and your state more than the headline yield. If you're comparing options across the market, it's worth seeing which crypto platforms support staking before assuming Coinbase is your best rate.

The state picture has improved since the 2023 enforcement wave. The SEC dismissed its case against Coinbase in early 2025, and five states — Alabama, Illinois, Kentucky, South Carolina, and Vermont — dropped their staking actions the same year, leaving California, New Jersey, Wisconsin, and Maryland as the holdouts. Staking is competitive for what it is, but the commission and the state restrictions matter more than the advertised rate. If you live in one of the four paused states, this isn't a reason to pick Coinbase.

Card

The Coinbase Card is a Visa debit card that spends your crypto balance with crypto-back rewards and no annual fee. It's a secondary feature rather than a reason to open an account on its own. The real cost is tax: every card swipe is a taxable disposal of crypto, which turns routine spending into a record-keeping job. For the full breakdown of fees, limits, and eligibility, see the Coinbase Visa Debit Card Review.

Wallet And Self-Custody Options

The Coinbase you trade on is custodial, meaning Coinbase holds the keys. Coinbase Wallet is a separate self-custody app where you hold the keys and the recovery phrase yourself, with access to onchain apps and more networks. The moment you move funds from the exchange into the Wallet, the safety net changes: Coinbase no longer controls those keys, recovery is on you, and a lost phrase means lost funds.

API And Programmatic Trading

Coinbase ships a full stack, which matters for active and institutional users and is irrelevant to a buy-and-hold beginner.

The API stack lifts the verdict for pro and institutional users, who also reach the lowest fee tiers. It doesn't change the calculation for someone using the consumer app.

Fees And Pricing

Coinbase is only cheap on one surface. Advanced Trade is competitive, and the simple-buy screen most beginners use is expensive enough to undo every other strength if you never switch off it.

Hidden Costs To Watch On Coinbase

This is where most users misread Coinbase. The low Advanced Trade fee table is real, but many beginners never use that screen. They buy from the main app, use Convert, or fund with a debit card instead, and the total cost ends up much higher than expected. Here's where the gap usually shows up:

- Main app simple buy: the quote can include both a visible fee and a built-in spread, so the real cost is usually higher than the headline fee line suggests.

- Debit card purchases: faster, but usually one of the most expensive ways to fund a Coinbase account.

- Convert tool: easy for swapping one coin into another, but the rate isn't the same as placing an order on Advanced Trade.

- Small crypto withdrawals: the fixed network cost hurts more on small sends, especially on Bitcoin and Ethereum.

- Perps and leveraged trades: beyond trading fees, the real risk is liquidation and ongoing position costs if the market moves against you.

The practical low-cost path on Coinbase is specific: deposit by free ACH, wait for funds to clear, place the trade on Coinbase Advanced, and withdraw on a lower-cost network when one is supported. For repeat buyers who still want the simple app flow, Coinbase One can reduce direct trading fees, though it doesn't make every trade free in practice since spread can still matter.

Coinbase One And Fee Discounts

Coinbase One is a subscription rather than a volume tier, and it only pays off at a specific usage level. The Preferred tier is $29.99 a month and waives simple-trade fees up to $10,000 of monthly volume, adds a 25% rebate on Advanced Trade fees, and includes $250,000 of account-compromise protection plus dedicated 24/7 support.

Spread can still apply on some flows, so the subscription only pays off if your monthly buys clear the fee you'd otherwise hand over. Good pricing on Coinbase isn't automatic. You either trade on Advanced Trade or pay the subscription to make the simple screen cheap, and the default experience is the costly one.

Deposits, Withdrawals, KYC And Availability

Funding and exit friction decide more of the experience than the feature list, and this is where Coinbase delivers for US users. Four things shape day-to-day use: funding, KYC, withdrawal limits, and state access.

What changes most is the method and your verification level. ACH is free but slow, instant RTP cash-out is fast and capped at $100,000 per transaction, and full KYC is mandatory before you can deposit, trade, or withdraw. For the full breakdown of US crypto exchange options if Coinbase doesn't fit your state or use case, the comparison is worth a look before you commit.

What US Users Need To Check Before Signing Up

US users should care more about feature access than headline availability, since Coinbase opens to nearly everyone but gates specific products by state. What matters is what you can actually do after approval.

Product access becomes uneven on staking specifically. Core trading and cash-out work the same everywhere, but a user in one of the four paused states can't stake new funds, so check that before you treat staking as a reason to join.

Payment Rails, Networks, And Limits

This section covers how Coinbase behaves once money starts moving: which rails are cheapest, which are fastest, and where a wrong-network mistake gets expensive.

Fiat Rails By Region

The best-value rail for most US users is ACH, which is free even though it's slower than the instant options.

Speed, cost, and availability split apart on the instant options. ACH costs nothing and takes days, while instant RTP cash-out is immediate and capped per transaction. This review scores the US market, where the rails work best.

Withdrawal Networks And Fees

A supported asset doesn't always mean a cheap network. Coinbase charges the network cost on crypto withdrawals, so the route you pick decides the fee.

The lowest-friction route for most users is a stablecoin on a low-cost network such as Base or Solana. Sending USDC over Ethereum when a cheaper network exists is the common, avoidable mistake.

Verification Levels And Withdrawal Limits

Coinbase uses identity verification rather than a long ladder of named tiers. What matters is the documents needed and the default limits, plus the extra checks that can appear after approval.

What usually triggers extra review is an unusual transfer pattern or a risk flag on the account, and this is the same mechanism behind the account-lock complaints covered later.

Is Coinbase Safe? Security, Custody And Proof Of Reserves

The direct verdict is that trust here is well-founded, and it rests on real structure rather than marketing. Coinbase is a US-listed public company with audited financials, a clean record on customer funds, and a cold-storage majority, which puts it near the top of our safest crypto exchanges rankings. The one honest limit is that no insurance covers a loss caused by someone compromising your own login.

Controls

Coinbase covers the controls that actually reduce account-takeover risk. It supports app-based 2FA and hardware security keys, passkeys, a security prompt, address allowlisting, and device and session management. The weak link is rarely the platform and usually a user whose own credentials are phished, which is exactly the case the crime policy doesn't cover.

Custody And Insurance

Crypto and cash get different protections, and the difference matters. Customer crypto is held mostly in cold storage with segregated custody, and a crime insurance policy covers a portion of held assets against theft and breach. USD cash works differently: it sits in custodial accounts at FDIC-insured banks and can qualify for pass-through FDIC coverage up to $250,000 per customer. That FDIC coverage applies to cash only and never to crypto.

Proof Of Reserves Or Audits

Coinbase runs a disclosure-led trust model, and for a listed company that's the better one. Instead of a Merkle-tree proof of reserves, it files audited financial statements with the SEC every quarter and year, reviewed by an external auditor, and reported $516 billion of assets on platform as of September 30, 2025. Audited public-company financials with segregated, regulated custody verify more than an assets-only reserve snapshot does. The two aren't the same thing, and Coinbase sits on the better side of that line.

Incidents And Remediation

Coinbase has no history of losing customer funds to a hack or insolvency, which is the record that matters most. It has had service outages during extreme volatility, and a 2025 data incident involving bribed overseas support contractors exposed some user data, which Coinbase disclosed and responded to. Neither event touched the custody of customer funds.

App, UX And Customer Support

The product experience is beginner-first, and that's both its strength and the source of its biggest cost. The app makes buying easy and keeps the cheap path slightly hidden. Support is the part that drags the score.

UI And Navigation

The interface is clean and built for newcomers, which is why so many people start here. The cost is that the default simple-buy screen is the expensive one, and Advanced Trade sits on a separate surface a beginner has to go find on their own.

- Beginner-first by default

- Cheap path lives on Advanced Trade

- Simple buy and advanced share one balance

Mobile App

The mobile app is highly rated and handles the core jobs well, letting a user fund, buy, sell, withdraw, manage security, and reach Advanced Trade from the phone.

- iOS and Android near parity with the web app

- Full funding and trading flows available on mobile

- Hardware-key and passkey support built in

Reliability And Status Page

Outages are easy to track but do still happen under load. Coinbase runs a public status page and posts incident notices, which gives users the transparency they want when something breaks.

Users generally get enough warning, with the exception of sudden load during sharp market moves, when the app has slowed or paused in the past.

Customer Support

Support looks built for self-service first and live help second, and that's the common complaint. The help center is deep, but reaching a person on the free tier is slow, and account locks are the issue users most often get stuck on. A few specifics worth knowing going in:

- Help center is thorough

- Live chat exists, but queues are slow

- Email and ticket support available

- Account locks are the top complaint

- Dedicated 24/7 line comes with Coinbase One

- Support can't reverse onchain sends once they're confirmed

Support quality is the clearest drag on the verdict. The platform itself is excellent, and the answer to a frozen account is often slower than it should be unless you pay for Coinbase One.

Coinbase Category Scores

These scores highlight how this review performs in specific categories, with each score tailored to the focus of that category.

Final Verdict

Coinbase's trust case is the strongest of any US retail exchange. Audited SEC financials, ~98% cold storage, segregated funds, and crime insurance on held assets give it a disclosure stack that most peers can't match. Free ACH and instant RTP cash-out up to $100,000 make the fiat experience frictionless for US users. The cost is the persistent caveat. The simple-buy screen is expensive, often 2.5% to 3.5% on small orders once spread is counted, and most beginners never switch off it. Advanced Trade brings fees down to 0.00%–0.40% maker and 0.05%–0.60% taker, which is competitive. Coinbase One removes simple-trade fees within a monthly cap for a subscription. Neither option is the default. Use Coinbase if you want the most regulated US exchange and plan to use Advanced Trade or Coinbase One. Skip it if you trade frequently on the default screen and won't switch.

US-listed public company (NASDAQ: COIN), ~98% of crypto held in cold storage, US-regulated perpetual futures

Why it stands out

- SEC filings show more than a Merkle-tree snapshot

- Native USDC with near-free withdrawals on Base

- Free ACH and instant RTP cash-out

- Among the largest US spot venues

- Clean tax exports and CoinTracker link

What to consider

- Simple buy carries a heavy spread

- Support is slow without Coinbase One

- Account locks are a recurring complaint

- New-fund staking paused in 4 states

Disclaimer: CryptoSlate may receive a commission when you click links on our site and make a purchase or complete an action with a third party. This does not influence our editorial independence, reviews, or ratings, and we always aim to provide accurate, transparent information to our readers.