What are credit spreads, why are they tight, and what does it mean for Bitcoin?

CryptoSlate's latest report dives deep into the concept of credit spreads and analyze their current state to understand their impact on the broader financial and crypto markets, especially on Bitcoin.

Introduction

Defined as the difference in yield between bonds with differing credit qualities, credit spreads are a barometer for the risk premium investors demand over risk-free assets. The nuances of these spreads are particularly pronounced between Investment Grade (IG) and High Yield (HY) bonds, where the disparity in yields reflects the underlying credit risk and investors’ appetite for such risks.

Monitoring credit spreads, especially in large economies like the U.S. and the E.U., is paramount for several reasons. First, they serve as a leading indicator of economic health, where tightening spreads may signal investor confidence and expanding economic activity. In contrast, widening spreads could foretell economic distress or heightened risk aversion.

In this report, CryptoSlate will dive deep into the concept of credit spreads and analyze their current state to understand their impact on the broader financial and crypto markets, especially on Bitcoin. We aim to show how these financial instruments reflect and also influence market dynamics, investor behavior, and, ultimately, the intersection between traditional financial markets and Bitcoin.

Understanding credit spreads

A credit spread represents the yield differential between two bonds of differing credit quality, essentially quantifying the extra return investors demand for bearing additional risk. This metric is instrumental in gauging the health and outlook of both the economy and financial markets.

The disparity in yields can be observed, most notably between Investment Grade (IG) and High Yield (HY) bonds. IG bonds are those rated BBB- or higher by major rating agencies, signifying lower risk and, consequently, lower yields. On the other hand, HY bonds, rated BB+ and below, carry a higher risk of default, offering higher yields to compensate investors for this increased risk.

Several key factors influence the dynamics of credit spreads, each influencing the overall market sentiment. Investors’ perceptions of the future economic landscape can significantly impact credit spreads. Optimism about economic growth tends to narrow spreads as the risk of default diminishes, whereas pessimism, often during recessions, widens them.

Central bank policies and the prevailing interest rate environment also play a crucial role. Rising interest rates can widen credit spreads by increasing borrowing costs, potentially heightening default risks for lower-rated issuers.

Inflationary pressures can lead to higher interest rates, affecting credit spreads similarly. Moreover, inflation erodes real bond returns, impacting investor demand and, consequently, credit spreads. The general mood and risk appetite of investors can directly influence credit spreads. In times of high uncertainty or market volatility, investors may flock to safer assets, widening spreads for riskier bonds.

Understanding these factors is critical for investors, especially in the crypto market, where traditional financial indicators like credit spreads can offer valuable insights into macroeconomic trends and investor behavior.

The current state of credit spreads

In the global financial market, credit spreads in the United States and the European Union hold paramount importance due to their broad implications on international finance and investment flows. These markets, being among the world’s largest economies, possess bond markets that are deeply integrated into the global financial system, influencing investor sentiment and capital allocation worldwide.

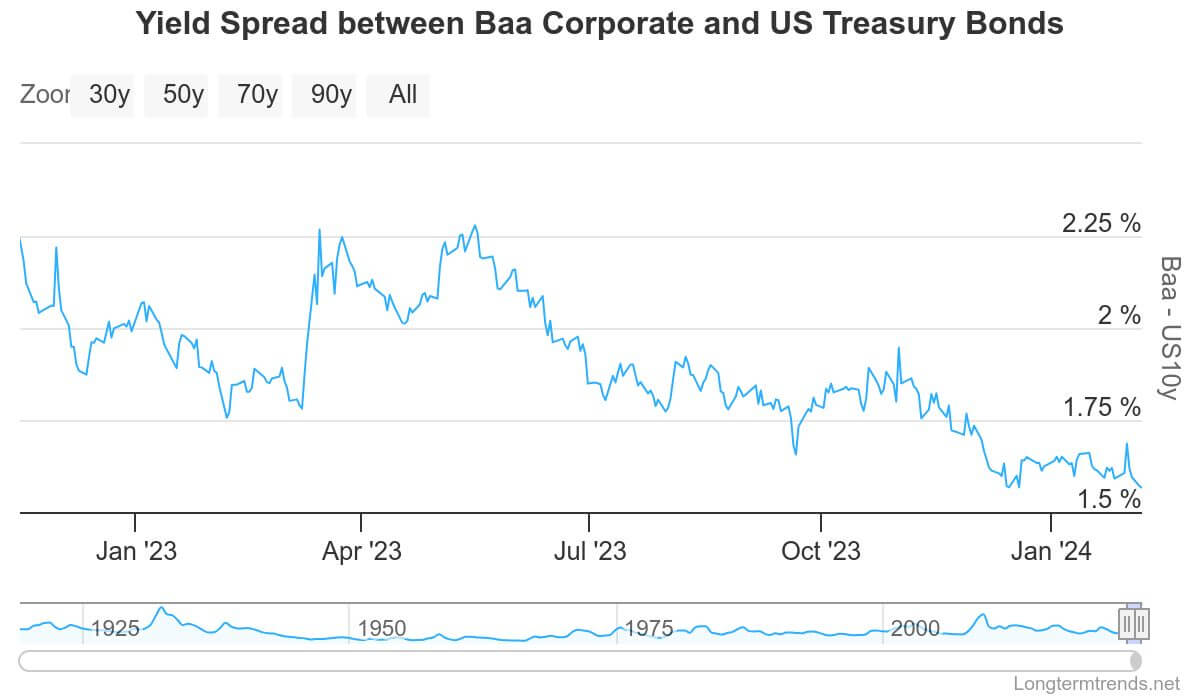

As of February 2024, credit spreads have notably tightened, a trend reflective of broader economic and monetary conditions. Specifically, the yield spread between Baa Corporate and U.S. Treasury Bonds, a benchmark for U.S. credit spreads, has contracted to 1.59% from 2.19% in May 2023.

This significant reduction underscores a marked shift in risk perception and investment preferences over the period. In the European context, the Euro IG and HY 12-month normalized spreads (z-score) moved from +0.5% at the end of 2023 to -2% in February 2024, indicating a similar compression in credit spreads.

The economic implications of tight credit spreads

In the E.U., tight credit spreads reflect a complex interplay of market sentiment, monetary policy, and economic indicators. While inflation is still well above the ECB’s target rate of 2%, the decline from its peak of 11.5% in October 2022 to 3.4% in December 2023 shows a gradual easing of inflationary pressure.

The ECB is keeping interest rates at record highs, with the main refinancing operations rate at 4.5% and the deposit facility rate at 4%. The Eurozone’s economic performance, particularly the stagnation in GDP growth in Q4 2023 and the contraction in the German economy highlights the fragile state of the regional economy. The risk of recession looms, albeit narrowly avoided, signifying a challenging economic environment.

The ECB’s high-interest rates, aimed at curbing inflation, can lead to tighter credit conditions as borrowing costs increase. In such an environment, tight credit spreads might seem counterintuitive unless investors perceive that the risk of default has not proportionately increased or that the return on safer assets (like government bonds) does not compensate for the lower perceived risk in corporate bonds. Investors may also anticipate a future monetary policy easing in response to stagnating economic growth, which could support bond prices.

Given the stagnating economy, investors might be driven towards corporate bonds over government securities to achieve higher yields, compressing the spreads despite the economic uncertainties.

This search for yield, especially in a context where recession fears are prevalent, suggests that investors are weighing the risks of corporate default against the backdrop of an economic slowdown and betting on continued support or intervention by the ECB if conditions worsen.

The tight credit spreads in this scenario could indicate that the market believes the ECB’s policies will successfully bring inflation down without causing a deep recession. Investors might perceive corporate bonds as relatively safe compared to the returns on government bonds, reflecting confidence in corporate resilience or in eventual policy shifts to support economic growth.

External factors such as global economic trends, geopolitical developments, or changes in commodity prices can also affect credit spreads. Investors might be reacting to a broader set of expectations about recovery or stability in global markets that could buffer the Eurozone economy against further downturns.

The current tightening of credit spreads in the U.S. is taking place against a backdrop of interesting economic conditions and policy responses. The U.S. economy has shown resilience and recovery from the pandemic-induced downturn, with growth stabilizing. Efforts to achieve a “soft landing,” despite challenges such as inflation and supply chain disruptions, have been somewhat successful, indicating a cautious but positive economic outlook.

The Federal Reserve’s policies to manage inflation, including adjustments to interest rates, have significantly influenced credit conditions. A tighter monetary policy to curb inflation has impacted borrowing costs and investor risk appetite, contributing to the observed credit spread dynamics.

Although inflation has been a central issue for the U.S. economy, recent trends suggest a gradual easing. This reduction in inflationary pressure, combined with strategic interest rate policies, has helped stabilize the economy and contributed to the tightening of credit spreads.

Discussions around the U.S. national debt and fiscal policy, including debates over the debt ceiling, have implications for market confidence and credit spreads. Investors are willing to accept lower premiums for corporate debt relative to risk-free government bonds, indicating optimism about corporate health and the overall economic outlook.

The effect of tight credit spreads on Bitcoin

The convergence of lower yield differentials in traditional bond markets has inadvertently highlighted the attractiveness of Bitcoin and Bitcoin ETFs as alternative investments for individuals and institutions from tradfi.

In periods of tight credit spreads, investors often find traditional fixed-income investments less appealing due to their diminished yields. This scenario has historically prompted a pivot towards alternative assets in pursuit of higher returns — including cryptocurrencies. Bitcoin always stood out as a particularly attractive option for investors, but a lack of regulated investment products always dampened the demand institutions, and tradfi investors had in the asset.

The general trend indicates that Bitcoin has often rallied during times of financial market uncertainty or when traditional yields were unattractive, showing that even this dampened demand had a noticeable effect on BTC.

The introduction of Bitcoin ETFs in the U.S. market has significantly altered this landscape. These financial instruments have allowed a broader spectrum of investors to gain exposure to Bitcoin’s potential returns without the complexities of direct cryptocurrency ownership.

As previously covered by CryptoSlate, the launch and growth of Bitcoin ETFs have been met with positive investor sentiment, evidenced by consistent inflows and the ranking of some Bitcoin ETFs among the largest commodity ETFs by assets held. This development shows the growing acceptance and institutionalization of Bitcoin as a legitimate investment class.

In the context of tight credit spreads, the diversification benefit and the non-correlated nature of Bitcoin’s returns relative to traditional assets make its inclusion in investment portfolios very compelling to large investors. Bitcoin ETFs enhance this proposition, providing a regulated, accessible, and efficient means for investors to hedge against inflation, currency devaluation, and other systemic risks inherent in traditional financial systems.

Conclusion

As delineated, credit spreads — the yield differentials between bonds of varying credit quality — serve not only as a gauge of perceived risk but also as a predictor of economic trends. The tight credit spreads in the U.S. and E.U. show an environment where investors are accepting lower yield premiums for riskier assets, influenced by accommodative monetary policies, economic recovery post-pandemic, and a constant search for yield amidst historically low interest rates.

This backdrop of tight credit spreads has consequential implications for the broader financial market and, notably, for Bitcoin and the nascent field of Bitcoin ETFs. As traditional investment yields become less attractive, Bitcoin emerges as a compelling alternative, offering the potential for higher returns and serving as a hedge against traditional financial market risks. The advent of Bitcoin ETFs further amplifies this attraction, providing a structured, regulated avenue for investment that bridges the gap between traditional financial markets and crypto.

More Market Reports