The economic implications of the Fed’s reverse repo (RRP) facility

CryptoSlate's latest market report dives deep into the intricacies of the RRP facility, exploring its impact on traditional financial markets and its potential effects on Bitcoin.

Introduction

The Federal Reserve’s Reverse Repurchase Agreement (RRP) facility is a critical yet often misunderstood component of the US monetary policy framework. Despite its significant impact on liquidity, interest rates, and financial stability, a considerable gap exists in understanding its mechanisms and broader market effects. This facility, designed as a monetary policy instrument, allows the Federal Reserve to withdraw excess liquidity from the financial system, thus helping to maintain the stability of interest rates and support the effective implementation of monetary policy.

The significance of the RRP facility has been underscored in recent years, notably during periods of quantitative easing and the COVID-19 pandemic, where it absorbed a substantial volume of excess liquidity to prevent negative interest rates.

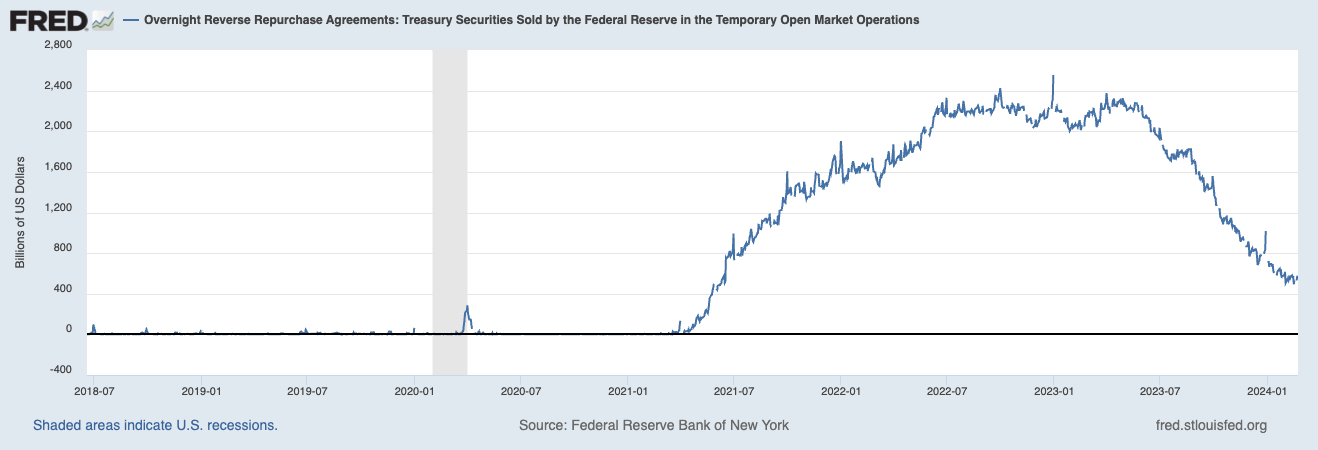

The scale of the RRP facility’s operations has reached unprecedented levels, with peak usage hitting around $2.5 trillion, highlighting its role as a key liquidity buffer for the financial system. Yet, despite its size and importance, misconceptions persist regarding its function and implications for the broader economy and financial markets.

In this report, CryptoSlate will dive deep into the intricacies of the RRP facility, explaining how it operates, exploring its historical evolution, and its increasingly important role in shaping monetary policy outcomes. We will explore its impact on traditional financial markets and its potential effects on the crypto ecosystem, particularly Bitcoin.

What is the Reverse Repurchase Agreement (RRP) facility?

The Reverse Repurchase Agreement (RRP) facility, operated by the Federal Reserve, is a financial instrument designed to manage liquidity in the banking system and steer short-term interest rates. In an RRP transaction, the Fed sells securities to eligible counterparties, such as money market funds, banks, and government-sponsored enterprises, agreeing to repurchase them at a predetermined price on a specified future date. This mechanism effectively withdraws liquidity from the financial system, acting as a tool for the Fed to control excess reserves and influence overnight interest rates.

Historically, the RRP facility has been pivotal during periods of significant banking system liquidity, serving as a safety valve to help maintain the Fed’s target interest rate range. For example, in the wake of the financial crisis of 2008 and subsequent quantitative easing measures, the Fed ramped up its use of RRPs to absorb the excess liquidity that resulted from its asset purchase programs. More recently, during the COVID-19 pandemic, the usage of the RRP facility surged to unprecedented levels, reflecting the immense liquidity injected into the markets through fiscal and monetary stimulus measures. Daily RRP take-up exceeded $2 trillion at certain points, underscoring the scale of excess reserves seeking a safe, short-term home.

A high RRP usage indicates that there is a surplus of liquidity in the financial system, as institutions opt to park their excess reserves at the Fed, often due to a lack of more attractive investment alternatives. Conversely, a low RRP take-up suggests tighter liquidity conditions, where financial institutions prefer to deploy their reserves in higher-yielding opportunities rather than with the Fed at lower rates. The dynamic shifts in RRP utilization offer insights into the broader market’s liquidity landscape and the prevailing economic sentiment.

The role of RRP in managing excess liquidity

The Reverse Repurchase Agreement (RRP) facility plays a crucial role in the Federal Reserve’s liquidity management strategy, particularly in the context of quantitative easing (QE) and its aftermath. QE, a policy through which the Fed purchases large quantities of securities to inject liquidity into the financial system, aims to lower interest rates and stimulate economic activity. However, this influx of liquidity necessitates a counterbalancing mechanism to prevent inflationary pressures and asset bubbles, a role the RRP facility adeptly fulfills.

During the COVID-19 pandemic, the Fed’s QE measures were amplified, leading to an unprecedented increase in bank reserves. Flush with cash, financial institutions sought safe, short-term investment options, significantly elevating the demand for the RRP facility. This was evidenced by daily RRP take-up rates reaching upwards of $2 trillion, a clear indicator of the sheer volume of excess liquidity in the system. By allowing financial institutions to park their excess reserves at the Fed, the RRP facility effectively helps to siphon off excess liquidity from the banking system, providing a floor under short-term interest rates and helping stabilize the financial markets.

The transition from QE to quantitative tightening (QT) intended to reverse the QE policies by reducing the Fed’s balance sheet and increasing interest rates. Despite the shift towards QT, the expected tightening of market liquidity was less pronounced than anticipated. Instead of being absorbed into productive economic activities or leading to significantly increased lending rates, the liquidity found its way back to the Fed through the RRP facility. This phenomenon suggests that while QT aimed to reduce the excess liquidity created by QE, the persistent high utilization of the RRP facility indicated a continued preference among institutions for the safety and liquidity provided by the Fed.

RRP’s impact on financial stability and the market

Quantitative tightening (QT), a process where the Fed aims to decrease its balance sheet and increase interest rates by selling securities, can potentially lead to increased market volatility and liquidity shortages. The RRP facility acts as a counterbalance to these forces by providing a mechanism for the Fed to absorb excess liquidity from the financial system, thus stabilizing short-term interest rates and maintaining orderly market conditions.

The impact of the RRP facility on financial stability is particularly evident when examining its relationship with bank reserves and the overall liquidity in the financial system. During QT, as the Fed sells off its holdings, there’s a natural decrease in bank reserves as financial institutions purchase these securities. However, the concurrent use of the RRP facility allows the Fed to manage the pace of this liquidity withdrawal effectively. By setting the terms at which it is willing to engage in reverse repos, the Fed can influence the amount of liquidity in the system, ensuring that short-term interest rates remain aligned with its policy objectives and preventing stress on the banking sector.

While the Reverse Repurchase Agreement (RRP) facility serves as a crucial tool for managing liquidity and fostering financial stability, it can also have unintended adverse effects on liquidity and broader financial markets under certain conditions. The RRP facility, by absorbing excess liquidity from the financial system, can inadvertently lead to a situation where there is insufficient liquidity for other market activities, particularly if the Fed’s actions are more aggressive than the market conditions warrant. This can happen when the rates offered by the Fed for RRPs are attractive enough to divert funds from lending and investment activities in the broader economy, potentially leading to tighter credit conditions and a slowdown in economic growth.

Moreover, a heavy reliance on the RRP facility can signal underlying issues in the financial system, such as a lack of confidence among market participants or an absence of viable investment opportunities. Such a scenario could lead to an over-consolidation of reserves within the Fed, as institutions prefer the safety of the RRP over riskier assets. While this might suggest stability on the surface, it could also indicate a broader aversion to risk that stifles economic innovation and growth. Additionally, in extreme cases, the concentration of activity within the RRP facility might create systemic risks if too many financial institutions become dependent on the liquidity it provides, making them vulnerable to sudden changes in the facility’s terms or the Fed’s monetary policy stance.

Furthermore, the impact of the RRP facility on short-term interest rates and the Fed’s ability to hit its target rate range can have mixed effects on the market. While the facility helps anchor the lower bound of the Federal Funds rate, an overly aggressive or poorly calibrated use of RRPs could distort the natural balance of supply and demand in the overnight markets, leading to volatility in short-term interest rates. Such volatility could increase the cost of borrowing for banks and corporations, impacting their investment decisions and operational costs.

The implication of RRP drawdown for the economy and markets

From an economic perspective, a reduction in the RRP balance can lead to an increase in bank reserves as funds flow out of the facility and back into the broader financial system. This increase in reserves can lower short-term interest rates, making borrowing cheaper and potentially stimulating economic activity. However, the effect on the economy depends on the banks’ willingness to lend and businesses’ and consumers’ desire to borrow.

If the RRP balance decreased but short-term rates remained unchanged, the expected stimulatory effect on the economy and financial markets could be significantly muted. In such a scenario, the liquidity ostensibly made available by the reduction in RRP balances might not effectively translate into increased economic activity or investment.

Under these conditions, the additional liquidity would likely remain within the banking system, leading to an accumulation of reserves without a corresponding increase in lending or spending. Furthermore, the situation could lead to distortions in the financial markets, with liquidity chasing a limited number of investment opportunities, potentially inflating asset prices without a solid foundation in economic fundamentals. This environment could heighten the risk of asset bubbles, where prices exceed their intrinsic value, increasing the susceptibility of markets to corrections and volatility.

Regarding Bitcoin, the implications of an RRP drawdown are nuanced. Bitcoin behaves as a risk-on asset, which means it can benefit from increased liquidity and risk appetite in the broader financial market, especially given the popularity of spot Bitcoin ETFs. As traditional market liquidity improves, some investors might seek higher returns in Bitcoin, driving up prices. However, the relationship is complex, as it also serves as a hedge against inflation and currency devaluation for some investors.

The connection between RRP, Fed’s policy, and the market

Changes in the RRP facility’s balance can serve as a barometer for liquidity conditions, influencing the Fed’s policy decisions and, subsequently, market behavior. When the Fed adjusts its RRP operations by increasing or decreasing the facility’s use, it sends powerful signals to the market regarding its stance on liquidity management and interest rate policies.

An increase in the RRP balance, signaling a withdrawal of excess liquidity from the market, often accompanies Federal Reserve policies aimed at tightening monetary conditions. This could involve raising interest rates or reducing the Fed’s balance sheet through quantitative tightening (QT). Such actions can lead to higher borrowing costs, potentially slowing economic growth and dampening investor sentiment. This can translate into reduced liquidity and increased volatility for the financial markets, including equities and cryptocurrencies, as investors recalibrate their expectations for growth and returns in a tighter monetary environment.

Conversely, a reduction in the RRP balance, indicating an infusion of liquidity into the financial system, could accompany or forecast a more accommodative monetary stance by the Fed, such as lowering interest rates or engaging in quantitative easing (QE). This scenario generally fosters a more favorable environment for borrowing and investing, potentially stimulating economic activity and buoying asset prices across the board, from stocks to real estate to crypto.

The impact of RRP and Fed’s policy on Bitcoin

Increases in the RRP facility’s usage, indicative of the Fed’s efforts to absorb excess liquidity from the market, often align with tighter monetary policies, including interest rate hikes or quantitative tightening (QT). Such policies can strengthen the dollar and increase yields on traditional financial instruments, making riskier assets like Bitcoin less attractive to investors seeking safe havens or higher returns. This scenario can exert downward pressure on Bitcoin’s price as the opportunity cost of holding non-yielding assets becomes more pronounced.

Conversely, a decrease in the RRP facility’s balance, signaling the Fed’s intent to inject liquidity into the financial system, can create a more favorable environment for Bitcoin. Accommodative monetary policies, such as lowering interest rates or engaging in quantitative easing (QE), decrease the yield on traditional investments, making Bitcoin’s proposition as a ‘digital gold’ or hedge against inflation more appealing. In such contexts, Bitcoin may see an influx of investment as market participants diversify away from traditional assets, potentially driving up its price.

Should the RRP balance decrease significantly in the context of economic strength and optimism, the resultant liquidity could fuel risk-on sentiment, benefitting Bitcoin as investors seek higher returns in alternative assets. If the depletion occurs amidst economic uncertainty or tightening financial conditions, Bitcoin could also benefit. Investors might initially seek refuge in safer assets, including cash or government securities, before turning to Bitcoin as a hedge against policy-induced market fluctuations or as part of a diversified investment strategy anticipating long-term gains.

More Market Reports