Disclaimer: The opinions expressed by our writers are their own and do not represent the views of U.Today. The financial and market information provided on U.Today is intended for informational purposes only. U.Today is not liable for any financial losses incurred while trading cryptocurrencies. Conduct your own research by contacting financial experts before making any investment decisions. We believe that all content is accurate as of the date of publication, but certain offers mentioned may no longer be available.

Crypto savings accounts continue to offer yields that traditional banks simply cannot match. However, the platform you choose has a direct impact on your returns, flexibility, and overall risk exposure.

Among centralized exchanges, Binance and CoinEx stand out as two popular options for earning passive income on crypto holdings. While both provide savings products with competitive APYs, they differ significantly in rate structures, liquidity, and asset coverage.

This guide explores how each platform works, compares APYs across major assets, and helps you determine which one aligns best with your investment strategy in 2026.

Binance Earn: Platform Overview and APY Structure

Binance organizes its savings products under its "Simple Earn" ecosystem, which includes both flexible and locked options.

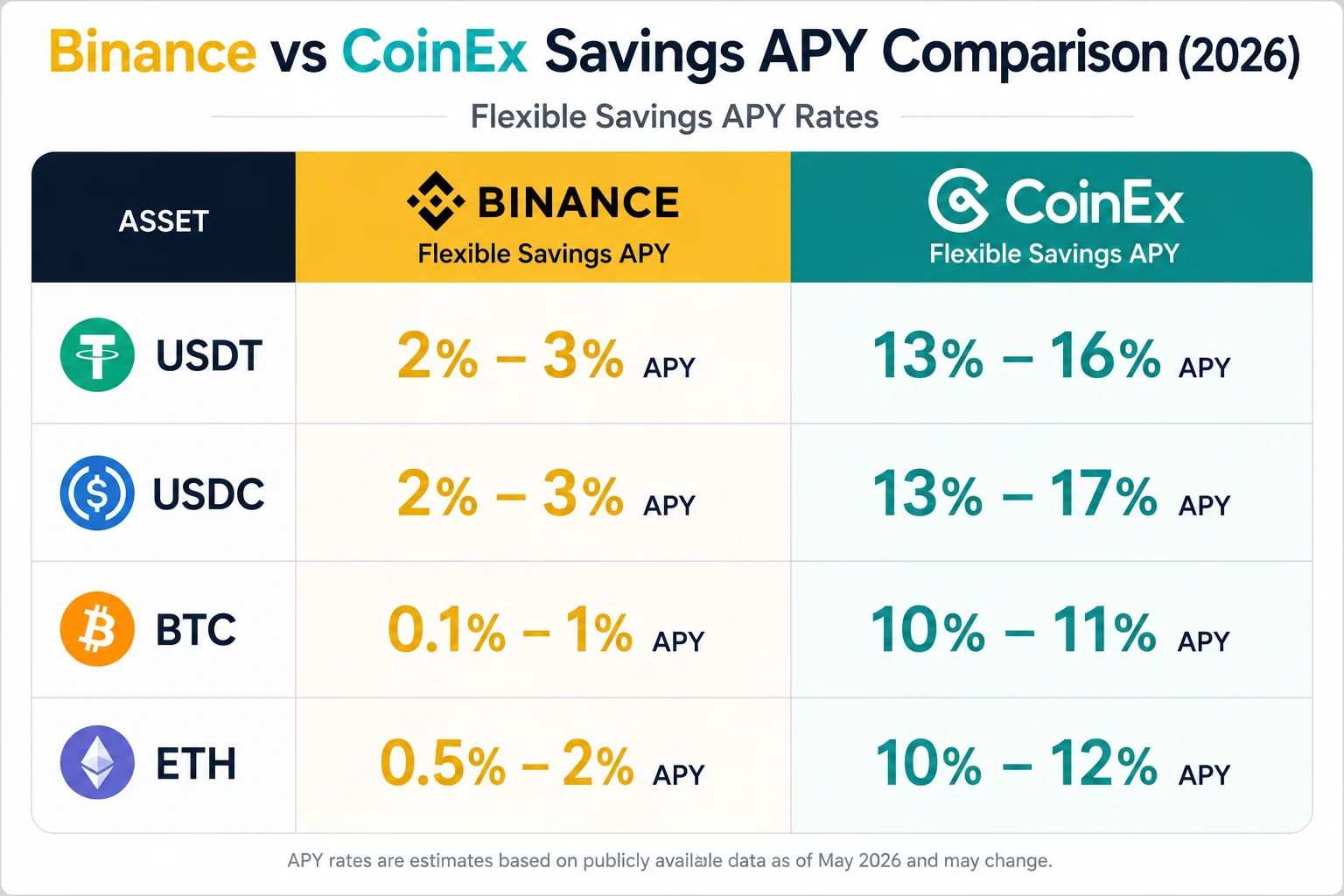

Flexible products on Binance offer relatively modest returns. Stablecoins such as USDT and USDC typically generate around 3% APY, while other assets range between 0.5% and 5%, depending on market demand. Interest is calculated daily and automatically compounded.

Locked products provide higher yields, particularly for stablecoins, which can reach up to around 8% APY depending on the term. Lock-up periods vary from 7 days to as long as 120 days. However, early redemption results in forfeiting all accrued interest.

One of Binance's key advantages lies in its extensive asset support. With over 300 cryptocurrencies available, users can diversify across a wide range of tokens, including major altcoins such as Cardano, Solana, and Polkadot.

CoinEx Earn: Platform Overview and APY Structure

CoinEx takes a different approach, focusing on higher yield generation through a revenue-sharing model. The platform redistributes a significant portion of earnings from margin lending and crypto loans back to users.

As a result, flexible savings rates on CoinEx are substantially higher than industry averages. Stablecoins such as USDT and USDC can generate around 13% APY, while Bitcoin and Ethereum deposits typically earn between 10% and 11%.

Interest on CoinEx is calculated hourly and credited daily, with compounding beginning after the initial period. Flexible funds can be redeemed instantly without penalties, making these products both high-yield and liquid.

APY Comparison: A Clear Gap in Yield

The difference in APY between the two platforms is significant and consistent across major assets.

For stablecoins, CoinEx's flexible rates around 13% dramatically outperform Binance's typical 2% to 3%. Even Binance's locked products often fail to match CoinEx's flexible returns.

A simple example illustrates this gap. A 1,000 USDT deposit could generate roughly 130 USDT annually on CoinEx, compared to about 30–50 USDT on Binance under standard flexible rates.

The same pattern applies to Bitcoin and Ethereum, where CoinEx consistently offers several times higher yields.

How Crypto Savings Accounts Work in 2026

What Are Crypto Savings Products?

Crypto savings accounts allow users to deposit digital assets and earn yield over time. Unlike traditional bank accounts, these returns are generated through mechanisms such as lending, staking, and participation in DeFi protocols.

In practice, platforms pool user deposits and deploy them into yield-generating activities. A portion of the returns is then distributed back to depositors as interest. Rewards are typically paid in-kind—for example, USDC deposits earn USDC.

It is important to note that these accounts are not protected by government-backed insurance schemes. Instead, safety depends on each platform's risk management, liquidity controls, and operational transparency.

Fixed vs Flexible Savings Models

Crypto savings products generally fall into two categories: flexible and fixed.

Flexible savings allow users to deposit and withdraw funds at any time. Interest accrues continuously, making these products suitable for users who want liquidity while still earning yield.

Fixed savings, by contrast, require users to lock funds for a specified period—typically ranging from 7 to 120 days. In exchange, platforms offer higher and more predictable returns. The trade-off is clear: higher APY comes at the cost of reduced liquidity.

How Platforms Generate APY

Most platforms rely on three core strategies to generate yield:

- Lending assets (especially stablecoins) to borrowers with collateral

- Staking assets on proof-of-stake networks

- Allocating funds to DeFi protocols

Higher APYs are usually associated with more aggressive capital deployment strategies, which can also introduce additional risks.

Get Started with High-Yield Savings

For users looking to take advantage of high flexible APY rates, CoinEx provides a straightforward entry point: https://www.coinex.com/en/flexible-earn

FAQ: Crypto Savings Accounts

What is a crypto savings account?

A crypto savings account allows users to deposit digital assets and earn interest through lending, staking, or DeFi strategies.

What is APY in crypto savings?

APY (Annual Percentage Yield) represents the annual return on an investment, including compounding.

What is the difference between flexible and fixed savings?

Flexible savings allow withdrawals at any time with lower APY, while fixed savings require locking funds for higher returns.

Conclusion

The comparison between Binance and CoinEx ultimately comes down to yield versus structure.

CoinEx leads decisively in APY, offering industry-highest APY, particularly for stablecoins and major cryptocurrencies. Binance, however, offers a more diversified and regulated ecosystem. Choosing the right platform depends on your individual goals, risk tolerance, and need for liquidity. For many users, a balanced approach that leverages the strengths of both platforms may offer the best overall outcome.

Dan Burgin

Dan Burgin