Bitcoin (BTC) climbed above $76,000 on April 14 after the Bureau of Labor Statistics reported March producer prices well below Wall Street estimates.

The data marked a sharp reversal from months of hotter-than-expected wholesale inflation prints, lifting risk assets and pushing BTC past a key institutional benchmark.

March PPI Misses on Every Measure

The Producer Price Index for final demand rose 0.5% month over month in March, less than half the 1.1% consensus forecast. Core PPI, which strips out food and energy, increased just 0.1% against a 0.4% estimate.

On a year-over-year basis, headline PPI printed 4.0% versus the 4.6% expected. Core came in at 3.8%, also below the 4.1% projection.

The miss followed back-to-back hot readings in January and February that had fueled stagflation concerns across macro and crypto markets.

Energy drove most of the remaining price growth. Final demand energy prices jumped 8.5%, with gasoline alone rising 15.7%. Meanwhile, food prices fell 0.3%, and goods excluding food and energy rose a modest 0.2%.

Bitcoin rallied past the $75,000 threshold to record an intra-day high of $76,038. As of this writing, BTC was trading at $75,335, up by almost 5% in the last 24 hours.

Strategy’s BTC Holdings Flip Profitable

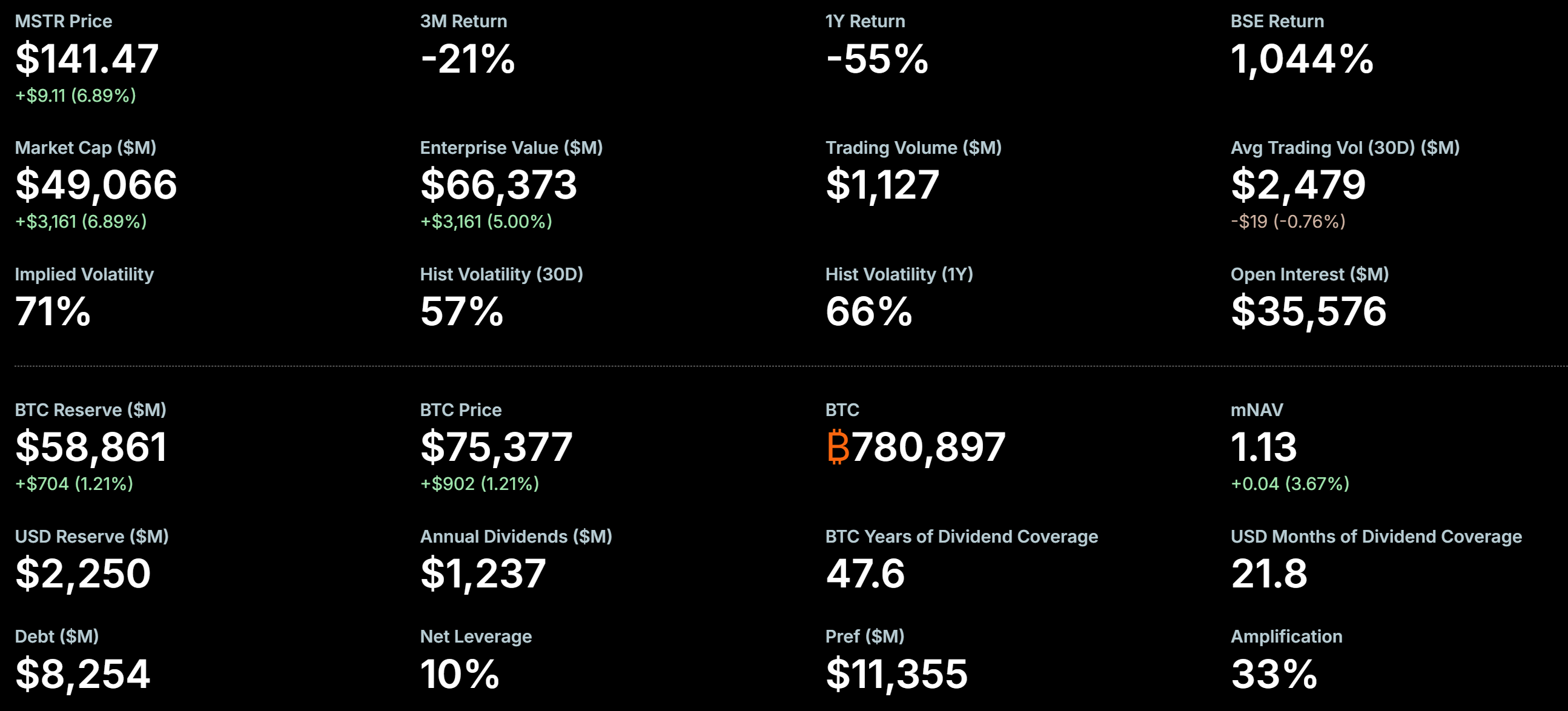

The price move carried significance beyond spot traders. BTC’s push to $76,038 took it above MicroStrategy’s average purchase price of roughly $75,580 per coin, turning the firm’s entire position profitable for the first time since late March.

Strategy holds approximately 780,897 BTC, making it the largest corporate Bitcoin holder. The company’s stock (MSTR) rallied 6.97% on the session to $141.58, and its Bitcoin reserve now carries a market value above $58.9 billion.

The firm had continued buying through April’s volatility, adding 4,871 BTC between April 1 and April 5 at an average price of $67,718 per coin.

That dip-buying strategy lowered its blended cost basis and positioned the portfolio for a quicker return to profitability.

Traders will now turn to Wednesday’s retail sales report and upcoming Federal Reserve commentary for signals on whether the cooler wholesale inflation trend will carry into consumer prices and rate-cut expectations.

If March CPI follows PPI lower, the case for a mid-year Fed pivot could strengthen considerably.